This study is aimed at analyzing factors affecting retail customers’ satisfaction when using m-banking services at Vietnamese commercial banks with Sacombank - Hanoi Branch being the main focus. Based on the theoretical framework of the SERVQUAL model developed by Parasuraman et al. (1988) and other relevant literature, this study identifies five major determinants of customer satisfaction when using m-banking consists of reliability, responsiveness, assurance, tangibility, and empathy. A survey was undertaken to collect primary data from 208 retail customers at Sacombank Hanoi Branch who have used Sacombank's m-banking services. Using Structural Equation Modeling, this study concludes that all five characteristics have a positive influence on satisfaction. Particularly, the five factors of reliability, responsiveness, assurance, tangibility, and empathy are found to have declining beneficial effects on satisfaction. Based on the analytical results, specific solutions and recommendations are proposed for the Hanoi branch in particular and Sacombank's head office in general in order to improve customer satisfaction when using m-banking services.

INTRODUCTION

Mobile banking has become increasingly popular in recent years due to its convenience and accessibility (Zedgenizova et al., 2021; Sadovnikova et al., 2022). Generally, this study defines m-banking based on the definition provided by Sacombank (2018): “M-Banking is online banking services on smartphones for transactions at anytime and anywhere by having access to the Sacombank mBanking application”. With the increasing use of mobile banking services, it is essential to understand the factors that influence customers' satisfaction with these services (Dorontsev et al., 2022; Hanawi et al., 2022).

Customer satisfaction when using services in general and mobile banking services, in particular, has been concluded as essential in many prior studies (Al-Zadjali et al., 2015; Khan et al., 2021; Nguyen & Phan, 2022). For commercial banks in Vietnam, mobile banking services are relatively new, and many customers may have hesitations about using them due to concerns about security, trust, and convenience (Nabavi & Gholizadeh, 2022). Studying customer satisfaction can help identify the factors that influence customers' perceptions of mobile banking services, address their concerns, and increase their trust, satisfaction, and loyalty to using the service (Biswas et al., 2023).

In Vietnam, it could be seen that consumers are gradually becoming familiar with the use of the Internet and online financial services on their mobile phones. The State Bank of Vietnam (2022) reported that electronic payments using mobile phones have been expanding quickly. Compare to the same period in 2021, smartphone transactions saw a 98.3% increase in volume and an 84.3% increase in value; QR code transactions saw an 86% and 127% increase in volume and value. The Ciovid-19 pandemic has boosted the technology adaptation process for Vietnamese consumers when using online services. Thus, it is advisable to study customer satisfaction when using m-banking services is essential for commercial banks to attract and retain customers.

In the attempt to investigate customers’ satisfaction when using mobile banking services in Vietnam, this study focuses on examining retail customers of Sacombank Hanoi Branch. During the development process, there are still many limitations in the quality of Sacombank’s m-banking services in particular compared to its competitors. There are issues with key operational indicators such as slow growth in the number of newly registered users, a decline in new account registration, and an increase in the inactive rate. Therefore, it is important to investigate current customers’ satisfaction with m-banking services provided by Sacombank to implement timely improvement and compete effectively with competitors.

There are relevant studies that focus on Sacombank’s electronic banking services, however, these early studies aimed at analyzing the intention to use instead of satisfaction (Tam, 2020; Hai & Nhan, 2021; Hong & Ly, 2022). However, as mentioned in the rationale, the Ciovid-19 pandemic has boosted the technology adaptation process for Vietnamese consumers when using online services. Thus, it is advisable to study customer satisfaction when using m-banking services has become more wildly accepted. Moreover, with regards to geographical scope, there has not been any prior study that investigates the customers’ satisfaction when using m-banking services at Sacombank Hanoi Branch in particular. Based on the aforementioned reasons, studying customer satisfaction when using mobile banking services is essential for Sacombank Hanoi Branch to improve its services, increase customer loyalty, and attract new customers.

Literature Review

Mobile Banking Services Quality

In existing studies, multiple service quality constructs are used to measure mobile banking (m-banking) customer satisfaction. Many studies have adapted the five SERVQUAL scales developed by Parasuraman et al. (1988) namely tangibles, reliability, responsiveness, assurance, and empathy to measure customers’ satisfaction with m-banking services (Al-Zadjali et al., 2015; Khan et al., 2021; Nguyen & Phan, 2022). Meanwhile, some other researchers included additional dimensions to measure customers’ trust such as security, and privacy (Arcand et al., 2017; Trialih et al., 2018; Owuamanam et al., 2022), and dimensions to measure the application quality such as design, aesthetic, ease of use (Arcand et al., 2017; Trialih et al., 2018; Owuamanam et al., 2022). Despite the differences, most of these newly developed constructs still lie under the generic SERVQUAL scale developed by Parasuraman et al. (1988). Moreover, the SERVQUAL scale of Parasuraman et al. (1988) has been applied in many m-banking satisfaction studies with high reliability and explanatory power (Al-Zadjali et al., 2015; Khan et al., 2021; Nguyen & Phan, 2022). Thus, based on these reasons, in this study, the scale of the SERVQUAL model of Parasuraman et al. (1988) is adapted to measure m-banking service quality.

Customer Satisfaction

Customer satisfaction arises from their perception of the value they obtained from their interaction with service providers or their transactions (Lam & Burton, 2005). According to Sathiyavany and Shivany (2018), satisfaction is the pleasure a customer has when he achieves the desired satisfaction and gets the advantages he anticipated, and satisfaction is the result of comparing what the consumer expects to get and what he anticipates obtaining. The customer's emotional reaction to their experiences is reflected in their satisfaction. It is associated with the goods or services he has acquired, and the emotional response is regarded to be the customer's responsibility as a result of the cognitive assessment and perception process of what the consumer thinks they receive. In the context of banking, satisfaction refers to customers' satisfaction with prior transactions or dealing experiences with a certain bank, which is also true in the context of Internet banking service quality (Anderson & Srinivasan, 2003).

In the context of electronic banking services, customer satisfaction is highly related to the overall quality of banking services. If the bank can improve the overall quality of banking services will be possible to satisfy customers and create customer loyalty (Thang & Long, 2013).

The Relationship between M-Banking Services Quality and Customer Satisfaction

This part of the study would review the major determinants in m-banking satisfaction, including tangibles, reliability, responsiveness, assurance, and empathy; while explaining their relationships with m-banking customers’ satisfaction.

To measure m-banking services quality, assurance has been used in many prior studies in recent years (Al-Zadjali et al., 2015; Khan et al., 2021; Nguyen & Phan, 2022). In the context of Vietnam, Nguyen and Phan (2022) discovered that assurance is anchored not only in the bank's staff's capacity to guide and advise clients on how to use mobile banking but also in the quality of the mobile banking app itself in serving consumers swiftly and accurately whenever they need it.

Prior research has found a substantial positive association between assurance and customer satisfaction while utilizing m-banking services (Al-Zadjali et al., 2015; Khan et al., 2021; Nguyen & Phan, 2022). Other studies focused on the dimension of security or privacy rather than assurance as a determinant of customer satisfaction when using m-banking services (Arcand et al., 2017; Ronny, 2022; Owuamanam et al., 2022). Security, like assurance, has a positive substantial link with consumer satisfaction with m-banking services (Arcand et al., 2017; Ronny, 2022; Owuamanam et al., 2022).

The second dimension of m-banking services quality is called responsiveness, which has been applied in many relevant studies (Al-Zadjali et al., 2015; Khan et al., 2021; Nguyen & Phan, 2022; Ronny, 2022). In general, responsiveness in m-banking quality is defined as 24-hour service, immediate response, available help, and gentle problem resolution (Hammoud et al., 2018; Thuy, 2019).

Prior research has established a substantial positive association between responsiveness and customer satisfaction when utilizing m-banking services (Al-Zadjali et al., 2015; Khan et al., 2021; Nguyen & Phan, 2022). Diversifying the traditional and online support systems will increase communication between banks and customers, thereby addressing interaction fairness and ensuring customers' interests (Dat & Cu, 2023). However, Ronny's (2022) research did not find a significant relationship between responsiveness and satisfaction when using m-banking services.

Another important factor to consider when evaluating the quality of m-banking services is empathy. Empathy is expressed through individualized service, making clients feel special and unique (Al-Zadjali et al., 2015; Khan et al., 2021). Thuy (2019) classed empathy in m-banking services as customer care, in line with prior studies. Nguyen and Phan (2022) defined m-banking empathy as the level of personalization, comprehension, and flexibility to client demands to fulfill both financial and psychological needs.

Previous research has found a positive relationship between empathy and customer satisfaction when utilizing m-banking services (Al-Zadjali et al., 2015; Thuy, 2019; Khan et al., 2021; Nguyen & Phan 2022). This outcome is consistent across research. Importantly, more human-related features, such as empathy, assurance, and responsiveness, have the biggest impact on consumer satisfaction with m-banking services in Vietnam.

Most studies define reliability in the context of m-banking as the ability to provide services exactly as promised, without errors, and within the agreed-upon time frame (Al-Zadjali et al., 2015; Trialih et al., 2018; Khan et al., 2021; Nguyen & Phan, 2022; Ronny, 2022). Despite having the same definition of delivering services on time, Owuamanam et al. (2022) referred to this dimension as fulfillment rather than reliability. Fulfillment characteristics include consistency with product availability, the capacity to modify and defer transaction processes at any moment without commitment, transaction correctness, and the ability to transmit information within a specified time frame.

Importantly, when it comes to m-banking services, reliability has a strong positive significant relationship with customer satisfaction. Several studies concluded that reliability was the most important determinant of customer satisfaction with m-banking services (Al-Zadjali et al., 2015; Trialih et al., 2018). This link is also found to be relatively strong in more recent investigations (Khan et al., 2021; Owuamanam et al., 2022).

The appearance of the mobile application interface, how information on the interface is transmitted, and whether the interface is appealing and intuitive will all influence how this is displayed in mobile banking. Nguyen and Phan (2022) concluded that some tangible characteristics of mobile banking services were the interface, design, and terms of mobile apps in terms of their appearance, convenience, and ease of use.

Prior research has found a positive significant link between tangibility and customer satisfaction when utilizing m-banking services (Al-Zadjali et al., 2015; Trialih et al., 2018; Nguyen & Phan, 2022). Other studies defined tangibility as ease of use (Trialih et al., 2018), design/aesthetics (Arcand et al., 2017; Ronny, 2022), and app design (Owuamanam et al., 2022). These tangibles comprise the overall consumer experience of using mobile banking services and are thus directly tied to customer satisfaction. In contrast, when applied in the context of Vietnam, the effects of tangibility were found to be insignificant in Nguyen and Phan's (2022) research. Nevertheless, given the recent increase in the speed of technological acceptance, it is still critical to re-evaluate the impact of tangibility on Vietnamese customers' satisfaction when using m-banking services.

MATERIALS AND METHODS

Research Model and Research Hypotheses

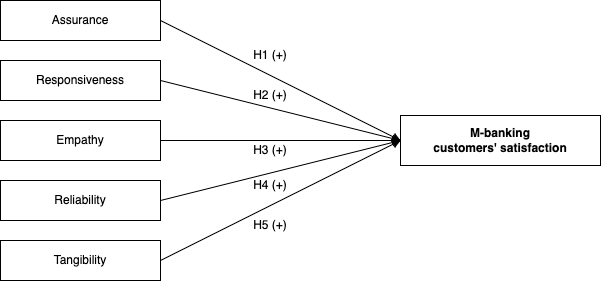

Generally, the five scales of the SERVQUAL model of Parasuraman et al. (1988) are adapted to measure the relationship between m-banking service quality and customers’ satisfaction including tangibles, reliability, responsiveness, assurance, and empathy. There are a total of five hypotheses and the research model is presented in Figure 1.

H1: Assurance positively influences customer satisfaction with m-banking services

H2: Responsiveness positively influences customer satisfaction with m-banking services

H3: Empathy positively influences customer satisfaction with m-banking services

H4: Reliability positively influences customer satisfaction with m-banking services

H5: Tangibility positively influences customer satisfaction with m-banking services

|

|

|

Figure 1. Research Model and Hypotheses |

Data Collection

Primary Data

All primary data was obtained via an online questionnaire created via Google Forms. The primary data collected includes two sections. The first section consists of demographic information such as age, gender, education level, monthly income, along with additional information on several banking apps used, and m-banking services used. The second section focuses on the factors affecting customer satisfaction with m-banking service quality.

Survey Sample

After collection, the responses were checked and removed if inconsistent or nonlogical answers were found. Here, nonlogical answers were those containing 100% homogeneous answers. A total of 243 responses were retrieved and 35 nonlogical responses were removed. Thus, 208 valid questionnaires were coded and used in the analysis. The requirement that the sample size must be equal to or more than 200 was also met by the number of valid questionnaires.

Data Analysis

Descriptive Statistics of Respondents' Characteristics

Table 1. Respondents' Profile

|

Category |

Group |

Frequency |

Ratio (%) |

|

Gender |

Male |

73 |

35.10 |

|

Female |

134 |

64.42 |

|

|

Other |

1 |

0.48 |

|

|

Age |

Under 25 |

53 |

25.48 |

|

25-35 |

98 |

47.12 |

|

|

36-45 |

41 |

19.71 |

|

|

46-55 |

9 |

4.33 |

|

|

Above 55 |

7 |

3.37 |

|

|

Education Level |

High School |

3 |

1.44 |

|

Bachelor Degree |

179 |

86.06 |

|

|

Master Degree |

16 |

7.69 |

|

|

Other |

10 |

4.81 |

|

|

Monthly Income (VND) |

Under 10M |

55 |

26.44 |

|

10M - Under 25M |

131 |

62.98 |

|

|

25M - Under 40M |

19 |

9.13 |

|

|

40M - Under 55M |

2 |

0.96 |

|

|

Above 55M |

1 |

0.48 |

|

|

Number of banking apps used |

1 app |

37 |

17.79 |

|

2 apps |

107 |

51.44 |

|

|

3 apps |

43 |

20.67 |

|

|

4 apps |

15 |

7.21 |

|

|

From 5 apps |

6 |

2.88 |

|

|

Services used on the Sacombank m-banking app |

Money Transfer |

204 |

98.08 |

|

Account Management |

156 |

75.00 |

|

|

Online Payment |

160 |

76.92 |

|

|

Online Savings |

127 |

61.06 |

|

|

Online Loan Services |

40 |

19.23 |

|

|

Card Services |

138 |

66.35 |

|

|

Shopping |

46 |

22.12 |

|

|

Buy Foreign Currency |

3 |

1.44 |

The Table 1 presented the demographic information of respondents in terms of gender, age, education level, and monthly income. There are 134 female respondents (64%) and 73 male respondents (35%) in the survey sample. Almost half of m-banking users are between the ages of 25 and 35 (more than 47%). Additionally, the majority of the respondents are well-educated, with nearly 86% holding a bachelor's degree. Almost 63% of the sample, have a monthly income of 10 million to under 25 million VND. For higher income levels, such as 25 million to less than 40 million VND per month, the number of respondents in this income bracket is slightly less, at 19 respondents (nearly 10%).

In addition to the demographic profile, the survey asks for the number of banking applications and the kinds of m-banking services respondents have used. Almost all of the respondents have used m-banking apps to transfer money, accounting for 98% of respondents. Meanwhile, the app's less frequently used features include online shopping, online loan service, and foreign currency purchase. Furthermore, approximately half of the sample reported using m-banking applications provided by two different banks (one from Sacombank and one from another). Interestingly, customers who are completely loyal to Sacombank and only use one app are represented in 37 responses, accounting for only 18%.

Reliability Analysis

Table 2. Cronbach's Alpha Results

|

Construct |

Item |

Corrected Item-Total Correlation |

Cronbach's Alpha |

|

AS |

AS1 |

0.692 |

0.919 |

|

AS2 |

0.866 |

||

|

AS3 |

0.849 |

||

|

AS4 |

0.853 |

||

|

EM |

EM1 |

0.692 |

0.899 |

|

EM2 |

0.768 |

||

|

EM3 |

0.780 |

||

|

EM4 |

0.764 |

||

|

EM5 |

0.750 |

||

|

REL |

REL1 |

0.735 |

0.857 |

|

REL2 |

0.689 |

||

|

REL3 |

0.775 |

||

|

RES |

RES1 |

0.466 |

0.794 |

|

RES2 |

0.737 |

||

|

RES3 |

0.626 |

||

|

RES4 |

0.606 |

||

|

TAN |

TAN1 |

0.777 |

0.901 |

|

TAN2 |

0.715 |

||

|

TAN3 |

0.837 |

||

|

TAN4 |

0.787 |

||

|

SAT |

SAT1 |

0.778 |

0.898 |

|

SAT2 |

0.845 |

||

|

SAT3 |

0.780 |

In the study, 208 questionnaires were analyzed using SPSS 26.0, the measurement model's reliability was evaluated through Cronbach’s alpha and Corrected Item – Total correlation. According to Table 2, it was found that Cronbach's alpha for each of the six variables fell between 0.794 and 0.919, which was higher than the threshold of 0.7 (Cortina, 1993). The corrected item-total correlation for each of the 22 observable variables was higher than 0.3 (Nunnally, 1978) Therefore, each of the six constructs met the criteria for exploratory factor analysis.

Exploratory Factor Analysis

Exploratory Factor Analysis (EFA) was conducted separately for independent and dependent variables. To ensure conducting EFA was suited to the study, three criteria were tested. Firstly, the Kaiser- Meyer- Olkin (KMO) must fall between 0.5 and 1, according to Kaiser (1974); and Bartlett's Test of Sphericity must also be significant to demonstrate that the observable variables were generally correlated with one another. Secondly, the scale is accepted when the Total Variance Explained is equal to or greater than 50% according to Anderson and Gerbing (1988). Thirdly, each observable variable must have a minimum Factor Loading of 0.5. These criteria demonstrate that the data used for Factor analysis is appropriate and the variables are correlated. All three conditions were satisfied in the EFA of independent and dependent scales. Notably, according to the Pattern Matrix in Table 3, there was a notable reassortment of elements for Assurance and Responsiveness. There were five main groups of factors that were extracted with RES1 integrated with the observable variables of the Assurance construct.

Table 3. Pattern Matrix Results

Extraction Method: Principal Axis Factoring.

Rotation Method: Promax with Kaiser Normalization.

a Rotation converged in 6 iterations.

Measurement Model Evaluation

Table 4. Results of Measurement Model Evaluation

|

CFA (n=208) |

|||

|

Path |

Outer loadings |

Composite reliability |

Average variance extracted |

|

AS1 à AS |

0.817 |

0.936 |

0.747 |

|

AS2 à AS |

0.917 |

||

|

AS3 à AS |

0.910 |

||

|

AS4 à AS |

0.908 |

||

|

RES1 à AS |

0.759 |

||

|

EM1 à EM |

0.795 |

0.926 |

0.713 |

|

EM2 à EM |

0.857 |

||

|

EM3 à EM |

0.867 |

||

|

EM4 à EM |

0.857 |

||

|

EM5 à EM |

0.846 |

||

|

REL1 à REL |

0.889 |

0.913 |

0.779 |

|

REL2 à REL |

0.852 |

||

|

REL3 à REL |

0.906 |

||

|

RES1 à RES |

0.894 |

0.886 |

0.723 |

|

RES2 à RES |

0.811 |

||

|

RES3 à RES |

0.843 |

||

|

TAN1 à TAN |

0.888 |

0.93 |

0.769 |

|

TAN2 à TAN |

0.854 |

||

|

TAN3 à TAN |

0.903 |

||

|

TAN4 à TAN |

0.862 |

||

|

SAT1 à SAT |

0.906 |

0.937 |

0.832 |

|

SAT2 à SAT |

0.935 |

||

|

SAT3à SAT |

0.896 |

||

The composite reliability, which can be read similarly to Cronbach's alpha in the PLS-SEM technique, was utilized as a way to gauge internal consistency. Nunnally and Bernstein (1994) claim that the acceptable composite dependability (CR) is more than 0.70. The CR value for each of the five constructs ranged from 0.886 to 0.937, as shown in Table 4. These results show that the measurements are reliable.

The average variance extracted (AVE) and the outer loadings were employed as two metrics to evaluate convergent validity. First, there should be an upper limit of 0.70 for the outer loadings (Hulland, 1999). The findings in Table 3 showed that every measurement item's outer loading was above the 0.70 threshold. Second, the AVE was employed as a gauge of common variance for a construct with a common threshold of at least 0.50. As a result, all five constructs had AVE values between 0.713 and 0.832, which satisfied the stipulation put out by Fornell and Larcker (1981).

The square root of the AVE of each latent variable should be greater than its maximum correlation with any other variable, according to the Fornell-Larker criterion, which was utilized to make the assessment. As a result, the results provided in Table 5 showed that all constructs had appropriate discriminant validity. All six factors—Assurance, Empathy, Reliability, Tangibility, and Satisfaction—were confirmed with high internal reliability and sufficient validity for the assessment of the structural model.

Table 5. Fornell-Larker Criterion for Discriminant Validity

|

CR |

AVE |

AS |

EM |

REL |

RES |

SAT |

TAN |

|

|

AS |

0.936 |

0.747 |

0.864 |

|||||

|

EM |

0.926 |

0.713 |

0.461 |

0.845 |

||||

|

REL |

0.913 |

0.779 |

0.561 |

0.553 |

0.882 |

|||

|

RES |

0.886 |

0.723 |

0.568 |

0.440 |

0.572 |

0.850 |

||

|

SAT |

0.937 |

0.832 |

0.669 |

0.607 |

0.724 |

0.700 |

0.912 |

|

|

TAN |

0.93 |

0.769 |

0.358 |

0.532 |

0.476 |

0.480 |

0.592 |

0.877 |

Note 1: AVE = Average variance extracted. The bold diagonal elements are calculated by the square root of the AVEs and non-diagonal elements are latent variable correlations.

Note 2: AS = Assurance, EM = Empathy, REL = Reliability, SAT = Satisfaction, TAN = Tangibility.

Structural Model Evaluation

The standardized root mean square residual (SRMR), the squared Euclidean distance (d-ULS), the squared geodesic distance (d-G), the normed fit index (NFI), and the root mean square residual covariance matrix (RMS_theta) were used in this study as model fit criteria for PLS-SEM. The results showed that all of the fit statistics were satisfactory (SRMR = 0.064, d-ULS = 1.121, d-G = 0.647, NFI = 0.803), with SRMR being less than the criterion of 0.5 (Byrne, 2001). According to Hu and Bentler (1998), an NFI value of 0.8 or above was regarded as appropriate for factor models. All of the values matched the fit criterion as recommended by Henseler et al. (2016), indicating a model that fit the data well.

To evaluate the structural model, the likelihood of predictor collinearity was first determined. According to Hair et al. (2014), when each predictor construct's tolerance or variance inflation factor (VIF) value is less than 5, the collinearity between the predictor constructs is at its lowest. The results showed that all inner model VIF values ranged between 1.589 and 1.961, indicating that there was no issue with the structural model's collinearity between the predictor constructs.

Table 6. Evaluation of Path Relationship

|

Paths |

Path coefficients |

T stats |

P stats |

Hypothesis Testing |

|

AS à SAT |

0.237 |

3.297 |

0.001 |

Accepted |

|

EM à SAT |

0.132 |

2.549 |

0.011 |

Accepted |

|

REL à SAT |

0.286 |

3.929 |

0.000 |

Accepted |

|

RES à SAT |

0.259 |

4.776 |

0.000 |

Accepted |

|

TAN à SAT |

0.176 |

3.878 |

0.000 |

Accepted |

The study used the PLS-SEM "bootstrapping" approach with 208 cases and 1000 resamples to generate t-values and p-values. Based on the results of Table 6, all five hypotheses were empirically supported. At a 1% significant level, it is confirmed that Assurance, Reliability, Responsiveness, and Tangibility have positive impacts on Satisfaction. At a 5% significant level, Empathy has a positive influence on Satisfaction. Among the five significant direct effects, Reliability had the greatest positive impact on Satisfaction (β REL → SAT = 0.286, p = 0.000), followed by Responsiveness (β RES → SAT = 0.259, p = 0.000), Assurance (β AS → SAT = 0.237, p = 0.001), Tangibility (β TAN → SAT = 0.176, p = 0.000), and finally Empathy (β EM → SAT = 0.132, p = 0.011). In addition, 72.5% of the variance in satisfaction was explained by the modeled factors. According to the generalization made by Henseler et al. (2009), this R2 value of satisfaction represented a moderate level of predictive accuracy.

RESULTS AND DISCUSSION

Overall, the results show that M-Banking satisfaction is positively influenced by reliability, responsiveness, assurance, tangibility, and empathy. All of these are consistent with prior studies. The results demonstrate that all five hypotheses are supported.

Firstly, reliability is the most significant determinant of M-Banking users’ satisfaction at Sacombank Hanoi Branch. Here, reliability is the capacity to supply services exactly as promised, without errors, and within the agreed-upon time frame. This also shows that the bank keeps its commitments to clients and meets their expectations through service outcomes. Customers' top priorities include timely and complete information (such as costs, usage, and promotions regarding Mobile banking), rapid and satisfying responses to any inquiries and complaints, confidentiality, security, and core functional value (as traditional banking services). With this result, it is also proven that Sacombank's brand image contributes to the level of service reliability, which in turns influence users’ satisfaction.

The second-ranked factor that influences customers’ satisfaction when using M-Banking services at Sacombank is responsiveness. The responsiveness in m-banking quality is determined by 24-hour service, immediate response, available support, and gentle problem resolution. For this study, responsiveness is measured in terms of both the application and the support staff. As for app responsiveness, customer satisfaction depends on fast transaction speed and 24/7 availability. As for personnel responsiveness, customers expect support to be offered around the clock and all complaints could be resolved professionally. Customers want to know exactly what is going on because of the high level of intangibility of service. With improvements in responsiveness, customers’ satisfaction when using Sacombank M-Banking services will also increase.

Along with responsiveness, the influences of Sacombank M-Banking services quality on customers’ satisfaction is rooted in the level of assurance. Assurance is the level of security and privacy that the services provide for its customers. Customers are satisfied with M-banking services when their sensitive information such as login details, accounts & card information is secured from external access, hacks, and frauds. Banks should provide their customers with data security when using m-banking services namely data encryption, client authentication, monitoring, and detecting aberrant activity. They should continuously improve customer perception of security concerns to maintain the safety and security of their customers. Thus, with higher assurance, users feel more protected when using Sacombank m-banking services, and become more satisfied.

Tangibility has positive impacts on M-Banking customer satisfaction. As mentioned in the literature review, tangibility in m-banking quality includes the interface, design, and applicable terms of mobile apps in terms of their appearance, convenience, and simplicity of use. Current Sacombank M-Banking customers express a clear negative attitude towards the tangibility of the service. Thus, to improve customer satisfaction, Sacombank needs to upgrade its user interfaces to make the app more user-friendly and aesthetic. The importance of the tangibility aspect was stated in the Annual General Meeting of Shareholders in April 2023, when the board of directors emphasized that digital transformation activities at Sacombank take the convenience of customers as the highest goal, focusing on four core factors: Technology infrastructure, Comprehensive digital solutions, Digital products and services, People and digital thinking.

Lastly, there is a positive significant relationship between empathy and customers’ satisfaction. This finding agrees with the prior studies carried out in Vietnam that risk-averse Vietnamese customers continue to expect individualized services, consultation, committed care, and highly attentive support from bank staff, even though the m-banking distribution channel can provide bank customers with greater autonomy in managing their banking transactions without direct support and response from staff despite the services is provided online. Specifically, offering mobile banking services which entails a high level of intangibility yet it still needs the backup of human-related factors from the front-line staff and technical staff. Thus, the more empathy customers gained from the services, the higher their satisfaction.

Based on the analytical findings, this study offered suggestions and solutions to enhance customer satisfaction when utilizing Sacombank m-banking services. Recommendations are supported by insightful information obtained from in-depth interviews with banking experts at the Sacombank Hanoi branch. The Sacombank Hanoi Branch is given two primary recommendations: (1) Maintain security and enhance trust through effective communication strategies and ongoing ethics training for staff, and (2) Increase empathy and responsiveness by enhancing consultation services to become more proactive and customized. In order to keep and attract consumers, Sacombank - Head Quarter should also (1) continuously improve its m-banking application, (2) strengthen its brand image, and (3) invest in promotional and marketing activities. Equally important, The State Bank of Vietnam must continue working with the Ministry of Public Security to (1) create a procedure for identifying and deleting "junk accounts," (2) encourage the use of population data, identification, and electronic authentication to support the country's digital transformation.

CONCLUSION

The study has successfully achieved its goals through the quantitative analysis of primary and secondary data. Based on the theoretical framework of the SERVQUAL model developed by Parasuraman et al. (1988) and other relevant studies, this study identifies five major determinants of customer satisfaction when using m-banking consists of reliability, responsiveness, assurance, tangibility, and empathy. A survey, on the other hand, was undertaken to collect feedback from 208 retail customers at Sacombank Hanoi Branch who have used Sacombank's m-banking services. The study concludes, using Structural Equation Modeling, that all five characteristics have a positive influence on satisfaction. Particularly, the five factors of reliability, responsiveness, assurance, tangibility, and empathy are found to have declining beneficial effects on satisfaction. Generally, customer satisfaction for the mobile banking distribution channel may be harder to achieve than for traditional banking services due to the integration of financial services and technology software. In order to remove ambiguity and foster consumer trust, Sacombank Hanoi Branch should work closely with its Head Quarter, under the instruction of the State Bank of Vietnam to implement solutions as proposed.

Limitations and Dimensions for Future Research

First of all, this study solely takes into account how variables affecting service quality influence how satisfied clients are with mobile banking services. Future studies should include the effect of geographical and demographic variables that could be related to mobile banking satisfaction.

Secondly, the final sample also reveals some sampling biases because Sacombank Hanoi branch clients were chosen as the source for data collection, and convenience sampling was used. Further research should therefore focus on other branches in Hanoi and other provinces as well, in order to deepen the significance of the results for Sacombank as a whole. Therefore, this research might either be expanded with more independent variables and control factors in other studies, or it could be redone with a larger sample size and improved representativeness.

ACKNOWLEDGMENTS: We express our heartfelt gratitude to all those who have contributed to this research paper, including our supervisors, collaborators, and supportive individuals. Without their invaluable contributions and support, this work would not have been possible.

CONFLICT OF INTEREST: None

FINANCIAL SUPPORT: The National Economics University supported this work.

ETHICS STATEMENT: None

Al-Zadjali, M., Al-Jabri, H., & Al-Balushi, T. (2015). Assessing customer satisfaction of m-banking in Oman using SERVQUAL model. In: Proceedings of the 2015 6th IEEE International Conference on Software Engineering and Service Science (ICSESS) (pp. 175-178).

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411-423. doi:10.1037/0033-2909.103.3.411

Anderson, R. E., & Srinivasan, S. S. (2003). E-satisfaction and e-loyalty: A contingency framework. Psychology and Marketing, 20(2), 123-138.

Arcand, M., PromTep, S., Brun, I., & Rajaobelina, L. (2017). Mobile banking service quality and customer relationships. International Journal of Bank Marketing, 35(7), 1068-1089. doi:10.1108/IJBM-10-2015-0150

Biswas, A., Jaiswal, D., & Kant, R. (2023). Augmenting bank service quality dimensions: moderation of perceived trust and perceived risk. International Journal of Productivity and Performance Management, 72(2), 469-490. doi:10.1108/IJPPM-04-2021-0196

Byrne, B. M. (2001). Structural equation modeling with AMOS: Basic concepts, applications, and programming. Routledge.

Cortina, J. M. (1993). What is coefficient alpha? An examination of theory and applications. Journal of Applied Psychology, 78(1), 98-104. doi:10.1037/0021-9010.78.1.98

Dat, P. M., & Cu, L. X. (2023). Research of customer satisfaction and loyalty with m-banking: Experience from equality theory. Journal of Economics and Development, 308, 42-51.

Dorontsev, A. V., Vorobyeva, N. V., Sergeevna, E., Kumantsova, A. M., Sharagin, V. I., & Eremin, M. V. (2022). Functional changes in the body of young men who started regular physical activity. Journal of Biochemical Technology, 13(1), 65-71.

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39-50.

Hai, D. T. T. & Nhan, L. T. T. (2021). Factors affecting decisions use mobile banking of personal customers at Saigon Commercial Bank Thuong Tin - Quang Tri Branch. Industry Trade Magazine, 12, 178-183.

Hair Jr, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

Hammoud, J., Bizri, R. M., & El Baba, I. (2018). The impact of e-banking service quality on customer satisfaction: Evidence from the lebanese banking sector. SAGE Open, 8(3). doi:10.1177/2158244018790633

Hanawi, S. A., Saat, N. Z. M., Hanafiah, H., Mohd Taufik, M. F. A., Nor, A. C. M., Hendra, A. K., Zamzuri, N., Nek, S., Ramli, P. A. M., Woon, S., et al. (2022). Relationship between Learning style and academic performance among the generation Z students in Kuala Lumpur. International Journal of Pharmaceutical Research & Allied Sciences, 11(3), 40-48.

Henseler, J., Hubona, G., & Ray, P. A. (2016). Using PLS path modeling in new technology research: Updated guidelines. Industrial Management & Data Systems, 116(1), 2-20. doi:10.1108/IMDS-09-2015-0382

Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. Advances in International Marketing, 20, 277-319. doi:10.1108/S1474-7979(2009)0000020014

Hong & Ly (2022). Factors affecting the intention of using Sacombank Pay. Scientific Journal of Ba Ria - Vung Tau University, 2(2), 51-60.

Hulland, J. (1999). Use of partial least squares (PLS) in strategic management research: A review of four recent studies. Strategic Management Journal, 20(2), 195-204.

Kaiser, H. F. (1974). An index of factorial simplicity. Psychometrika, 39(1), 31-36.

Khan, A. G., Lima, R. P., & Mahmud, M. S. (2021). Understanding the service quality and customer satisfaction of mobile banking in Bangladesh: Using a structural equation model. Global Business Review, 22(1), 85-100. doi:10.1177/0972150918795551

Lam, R., & Burton, S. (2005). Bank selection and share of wallet among SMEs: Apparent differences between Hong Kong and Australia. Journal of Financial Services Marketing, 9(3), 204-213.

Nabavi, S. S., & Gholizadeh, B. (2022). Evaluation of the quality of life of the patients with heart failure in Ahvaz teaching hospitals. Entomology and Applied Science Letters, 9(1), 26-30.

Nguyen, M. P., & Phan, A. (2022). Customer satisfaction about mobile banking distribution channel in Vietnamese commercial banks. Journal of Distribution Science, 20(8), 69-79.

Nunnally, J. C. (1978). Psychometric theory. New York: McGraw-Hill.

Nunnally, J. C., & Bernstein, I. H., (1994). Psychometric theory. McGraw-Hill, New York.

Owuamanam, J. N., Abdullah, S., Jusoh, Y. Y., & Pa, N. C. (2022). E-Service quality model for assessing customer satisfaction of mobile banking service. In 2022 Applied Informatics International Conference (AiIC) (pp. 178-183). IEEE. doi:10.1109/AiIC54368.2022.9914577

Parasuraman, A., Zeithaml, V., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12-40.

Ronny, (2022). The effect of responsiveness, reliability, ease, security, and aesthetics on customers’ satisfaction using mobile banking. International Journal of Economics, Business and Management Research, 6(7), 190-205. doi:10.51505/IJEBMR.2022.6713

Sadovnikova, N., Lebedinskaya, O., Bezrukov, A., & Davletshina, L. (2022). The correlation between residential property prices and urban quality indicators. Journal of Advanced Pharmacy Education & Research, 12(2), 98-103.

Sathiyavany, N., & Shivany, S. (2018). E-Banking service qualities, E-Customer satisfaction, and e-loyalty: A conceptual model. The International Journal of Social Sciences and Humanities Invention, 5(6), 4808-4819.

Tam, N. Q. (2020). Factors affecting the intention to use e-banking services of individual customers at Sacombank. Industry Trade Magazine, 1(1), 284-293.

Thang, T. Đ., & Long, P. (2013). The relationship between e-banking service quality and customer satisfaction and loyalty in Vietnam. Journal of Economics and Development, 195, 26-33.

Thuy, B. V. (2019). Factors affecting individual customers' satisfaction with e-banking services of commercial banks in Dong Nai. Lac Hong Science Journal, 8, 8-13.

Trialih, R., Astuti, E. S., Azizah, D. F., Mursityo, Y. T., Saputro, M. D., Aprilian, Y. A., & Rizki, A. S. (2018). How mobile banking service quality influence customer satisfaction of generation x and y? In 2018 International Conference on Information and Communication Technology Convergence (ICTC) (pp. 827-832). IEEE. doi:10.1109/ICTC.2018.8539720

Zedgenizova, I., Ignatyeva, I., Zarubaeva, E., & Teplova, D. (2021). IT opportunities: Increasing the level of financial security in digital economy. Journal of Advanced Pharmacy Education & Research, 11(3), 157-161.