The purpose of this research is using the Analytical Network Process to help organizations with Internal Auditor Selection. The researcher, drawing on all of the systematic extrapolation and deductive scientific research, and after that the researcher to the model proposed in final form, its application to one of the companies listed in Egyptian Stock Exchange as a case study. And through the relative weights of the three alternatives in terms of the main and sub-factors for choosing the internal auditor and this led to the first alternative, related to Insourcing, ranked first with a rate of 39.20%. and The second alternative, related to Outsourcing, ranked third with a rate of 23.43%. and The third alternative, related to Co-Sourcing, ranked second with a rate of 37.36%. And the researcher also performed an Sensitivity analysis of the results of applying the proposed model, and that used the Plot map the sensitivity test by applying the second main factor (neutrality, independence, and objectivity). and that it is when increasing the relative importance of the second main factor in the proposed model for the third alternative compared to the second alternative from 1/2 to 4, where that led to me to a change in the order of the alternatives from what it was the situation before making the change.

INTRODUCTION

The Institute of Internal Auditors defines internal auditing as "Internal Auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes" (The Institute of Internal Auditor, 2009).

Since this definition did not specify the source of the internal auditor, whether it was from the inside or from the outside, which opened the way for the body responsible for selecting and appointing the internal auditor, three alternatives to appointing the internal auditor, either from the inside or from the outside or both.

Therefore, the researcher sees the need to search for a new method that helps in choosing the internal auditor in a way that prevents or limits the problems that avoid the previous alternatives and is in line with the needs of the establishment. Perhaps one of the most prominent methods that help in choosing between alternatives and the most widespread is the process of network analysis and the process of hierarchical analysis.

The analytic network process (ANP), a generalization of the analytic hierarchy process (AHP), is a decision analysis methodology that employs a set of axioms to develop a hierarchy of attribute values, based on the relative values obtained from pairwise comparisons of attributes. The ANP has advantages in the analysis, synthesis, and justification of complex decisions (Jeong, 2020). Decision-makers have to judge each element, and the judgments are made on the basis of decision-makers' experience and knowledge (Kyavars, 2021).

The analytic network process is one of the multi-criteria decision-making methods widely used to solve various issues in the real-world due to the consideration of complex and interrelated relationships between decision elements and the ability to apply quantitative and qualitative attributes simultaneously (Kheybari et al., 2020; Zandieh, 2020).

Four major steps of ANP are (1) model construction, (2) pairwise comparison matrices and priority vectors, (3) supermatrix formation, and (4) selection of the best alternative (Jeon et al., 2017).

Previous Literature

The topic of selecting and appointing the internal auditor has received remarkable attention from researchers, especially after the issuance of the contemporary concept of internal auditing, which made it possible for the external auditor to carry out the work of internal auditing. Which opened the way for many studies that dealt with the selection and appointment of internal auditors, and among these studies: (Sobeihi, 2000; Abdel-Fattah, 2001; Aldhizer et al., 2003; Ahlawat & Lowe, 2004; Mohamed, 2004; Mujahid, 2006; Abbott et al., 2007; Mansour, 2007; Brandon, 2010; Al-Rifai, 2012; Emara, 2012; Salem, 2012; Inua & Abianga, 2015).

Several studies dealt with the use of the hierarchical or network analysis process to support multifactorial complex decision-making in many areas and achieved impressive results in achieving this support in those areas and among these studies: (Saaty, 1994; Al-Adwani, 2001; Saaty & Vargas, 2001; Cheng & Li, 2004; Bahrams, 2005; Percin, 2006; Lin & Hsu, 2007; Al-Shobaki, 2008; Hsu & Chen, 2008; Akl, 2010; Hadid, 2012; Punniyamoorty et al., 2012; Shaverdi & Barzin, 2012; Daim et al., 2013; El-Garhy, 2013; Brunelli, 2015; Farooq & Moslem, 2020; MirarabRazi et al., 2020; Özdemir, et al., 2020; Zarei et al., 2020).

Concerning the studies that dealt with the use of the hierarchical or network analysis process, or both of them together, in the selection and appointment of the internal auditor, we find a study (Seol & Sarkis, 2005) that proposed an ideal model for selecting internal auditors using the multiple attributes analysis method, and the aim of this The study is to assist organizations in selecting and evaluating internal auditors by introducing several multiple attributes more effectively, using the hierarchical analysis process, which has been used in several fields to make an administrative decision.

Another study (Sarkis & Seol, 2006) used the integration between the Analytical Network Process and the Analytical Hierarchy Process in the selection of the internal auditor. This study aimed to consider it as an introduction to a more robust model by using the integration between the Analytical Network Process and the Analytical Hierarchy Process in the selection of the internal auditor, which includes the interdependence and interdependence of the various criteria for selecting employees, factors, and possible alternatives.

Another study (Dağdeviren & Yüksel, 2007; Alghamdi et al., 2021) used the Analytical Network Process in staff selection, as in the literature there are different methods regarding staff selection. However, it is noted that in these methods the interdependence of personnel selection factors is not taken into account. In this research, a method was studied that includes the factors of the interdependence of the factors of employee selection first, then the factors eligible for acceptance as criteria in selecting employees are determined, and a decision-making model is developed that indicates the dependency between these factors. The global weights of the factors in the model are estimated through the Analytical Network Process. Second, a scale is constructed to evaluate the factors for employee selection. Finally, how the adequacy of applicants can be measured is illustrated as an example.

It is clear from the previous presentation of the most important studies related to the topic that although the studies conducted by Inshik and Joseph focused on the selection of the internal auditor by appointing an employee from within the company itself, and therefore the current study differs from what was done by Inshik and Joseph, and that Because the current study is a comparison between the selection and appointment of the internal auditor as an employee from the inside - as in the previous studies - or from the outside or both.

After several previous studies were dealt with, it was concluded that the Analytical Hierarchy Process may be deficient, and therefore it is possible to benefit from the Analytical Network Process to avoid the shortcomings in the Analytical Hierarchy Process. Perhaps the main difference between the Analytical Hierarchy Process and the Analytical Network Process is that the importance of criteria has been derived The available alternatives, using feedback, and therefore was not determined from top to bottom in an abstract manner, that is, the focus should be on the priorities of the criteria from the alternatives through feedback rather than their importance to the goal.

The research problem can be formulated through the following questions:

Research Objective

The main objective of this research is to build a proposed model for selecting the internal auditor using the Analytical Network Process. This goal can be divided into several sub-goals, as follows:

Research Hypothesis

To achieve the research objectives, the following hypothesis will be tested:

The use of the Analytical Network Process leads to rationalizing the decision to select the internal auditor.

MATERIALS AND METHODS

In this study, the researcher depends on the use of both the deductive method and the inductive method by analyzing what was mentioned in books and periodicals, whether Arab or foreign, and what was mentioned in laws, legislation, and publications related to the profession and any other sources of knowledge to elicit points and criteria related to the topic of research. And applying what will be reached regarding the proposed model to one of the joint-stock companies listed on the Egyptian Stock Exchange as a case study, to help rationalize the decision of selecting and appointing the internal auditor.

Steps to Build the Proposed Model for Selecting the Internal Auditor

To Build a Model for Selecting the Internal Auditor, the Researcher Believes that this Requires Four Basic Steps, Namely

The First Step: the hierarchical and network construction by defining the differentiation factors between the alternatives (choice factors), as well as defining the available alternatives (selection alternatives).

First: Determining the Differentiation Factors between the Alternatives (Selection Factors)

The researcher believes that the selection factors are divided into main factors, including several sub-factors, and the following deals with these factors: (Elgendy, 2015).

The First Major Factor: the qualities and characteristics of the internal auditors:

The qualities and characteristics that must be available in internal auditors can be summarized in two types of skills, as follows:

The Second Major Factor: impartiality, independence, and objectivity.

The Third Major Factor: fees.

The Fourth Major Factor: Providing new services following the contemporary concept of internal auditing, which is represented in:

- Evaluate the efficacy and improvement of risk management processes.

- Evaluate and improve control and governance processes.

- Consulting and Assurance Services.

The researchers believe that the selection factors are divided into main factors, including several sub-factors, and the following deals with these factors: (Elgendy, 2015).

Second: Determining the Available Alternatives (Choice Alternatives)

It was clear from the definition of internal audit that three alternatives were drawn for selecting the internal auditor, which are:

The First Alternative: Insourcing: The internal audit is carried out by auditors working in the facility itself, that is, it takes place inside the facility with the knowledge of some of its employees who are assigned by the facility’s management to carry out this task.

The Second Alternative: Outsourcing: assigning one of the audit offices to carry out the entire internal audit work.

The Third Alternative: Co-Sourcing: by assigning one of the audit offices to perform the internal audit work incompletely, in addition to the presence of an internal audit department that undertakes the rest of the work, that is, there is a cooperation between the external auditor and the internal audit department.

The Second Step: the binary comparison between the main factors each other as well as the sub-factors with each other, and then weighing them concerning the goal. Where the degree of importance between two factors is measured by the verbal and numerical method. If the comparison is made by a group of experts, the geometric mean of each comparison between two factors is taken.

But before making binary comparisons between the factors and each other, and since the Analytical Hierarchy Process has deficiencies in that it does not measure the internal relationships between the factors and each other, and to avoid this, the integration between the Analytical Network Process and the Analytical Hierarchy Process is utilized to consider all the relationships between elements and some of them, some of the main and sub-factors.

And Table 1 shows the relative importance scale according to the classification of Saaty: (Saaty, 2008).

Table 1. The relative importance scale

|

Interpretation with a verbal analogy |

the definition |

Digital Weight |

|

The two factors are of equal importance |

Equal in importance |

1 |

|

One of the two factors is moderately more important than the other |

moderate importance |

3 |

|

One of the two factors is more important than the other |

great importance |

5 |

|

One of the two factors is much more important than the other |

very important |

7 |

|

One of the two factors is more important than the other |

utmost importance |

9 |

|

Average values used between previous weights when numerical comparison |

Intermediate importance between the above-mentioned values |

2,4,6,8 |

|

It is necessary to make a comparison by choosing the smallest of the elements as a unit to estimate the largest elements as a double of that unit |

If an activity (x) has one of the above correct values when compared to activity (y), then activity (y) takes the reciprocal of that value when compared to activity (x). |

The reciprocal of the above values |

|

If compatibility and stability are assumed by obtaining (n) numbers from the numerical values of the matrix expansion |

The resulting ratio of the scale |

logical functions |

|

When the elements are close to each other, and it is almost difficult to distinguish between them, the value of the moderate is equal to (1,3) while the value of the extreme is (1,9) |

For very similar activities |

(1,1 – 1,9) |

That matrix is prepared for each of the main factors with their sub-factors, as well as the sub-factors with other sub-factors.

Naturally, to achieve acceptable results, in reality, there is a need for a certain degree of consistency in calculating priorities for elements or activities based on certain criteria. The Analytical Hierarchy Process measures the total consistency of judgments by calculating the consistency ratio. The stability ratio should be (10%) or less (in fact, 5% for 3 × 3 matrix, 9% for 4. 4 matrix, and 10% for larger matrices). If the stability ratio is higher than (10%), it means that the judgments are somewhat random and must be reviewed. (Saaty, 2000).

The Consistency Ratio is determined as follows: (Al-Rashed, 2011).

|

|

(1) |

Where: CR = Consistency Ratio.

CI = Consistency Index.

RCI = Random Consistency Index. And you can write RI directly.

The Consistency Index is determined as follows: (Katarne & Negi, 2014).

|

|

(2) |

Where: CI = Consistency Index.

λ Max = Eigenvalue for the matrix of binary comparisons.

N = the number of factors being compared.

The Table 2 shows the values of the random Consistency index, as follows: (Triantaphyllou & Mann, 1995; Bagla et al., 2013).

Table 2. The values of the random Consistency index

|

10 |

9 |

8 |

7 |

6 |

5 |

4 |

3 |

2 |

1 |

N |

|

1.49 |

1.45 |

1.41 |

1.32 |

1.24 |

1.12 |

0.90 |

0.58 |

0 |

0 |

Random Consistency Index (RI ) |

The Third Step: making binary comparisons between the decision alternatives with each other, and then measuring their relative weight about the main and sub-selection factors and measuring the degree of stability, then a preference matrix is made for each of the alternatives, in terms of each factor, and the preference vector is determined to determine the relative weight of each alternative for each factor.

The Fourth Step: evaluate each alternative concerning each of the selection factors and test the sensitivity of the model, where the best alternative is selected by finding the sum of the product of the relative weight of the alternative in the total relative weight, then conducting a sensitivity test for the model, by changing the preference vector for the main selection factors, to show the effect of the alternative when changing the relative importance of one of the main selection factors.

Application of the Proposed Model for Selecting the Internal Auditor (Case Study)

In this part, the researcher applies the proposed model to help rationalize the decision to choose the internal auditor, through a comparison between three available alternatives, which is that the internal auditor should be from the inside or the outside, or a mixture of the inside and the outside.

The Company Under Study

The case study was conducted on El Sewedy Electric Company. El Sewedy Electric Company was founded in 1938, where it began its business by marketing electrical supplies, and flourished in becoming into one of the leading companies in the energy sector in the Egyptian market, and its activities in many international markets. The company has expanded its business beyond the Egyptian market by using its extensive experience in the production of diverse electrical products and its in-depth knowledge of the regional markets in which it functions. The company contains five main divisions of cables and wires, meters, electrical activities, electrical transformers, and projects and development. This base serves large customers from industrial and commercial companies to individual customers. (http://ir.elsewedyelectric.com/ar/company-overview)

Study Population and Sample

The study population and sample consist of members of the Board of Directors and members of the Audit Committee of El Sewedy Electric Company.

The Program Used to Enter the Data and Measure the Factors Used in the Model

The data was entered into the Super Decisions program, to perform the calculations and calculate the relative weights of the main and sub-factors to reach the general model for selection and determine the best alternative that gets the highest evaluation.

The program calculates the stability percentage in the data that is entered to ensure that it will not exceed 10%. In the event of something else, the input is reviewed again with the members of the Board of Directors and members of the Audit Committee.

Data Entry Methods in Super Decisions

The Super Decisions program is characterized by the multiplicity of data entry methods, and the researcher believes that this multiplicity may be intended to be used by individuals who face the problem of making a decision that has several alternatives according to the easiest way for them, and the methods used are represented in five methods represented in the direct entry method, and Questionnaire Mode, Matrix Mode, Verbal Mode, and Graphic Mode.

Applying the Proposed Model for Selecting the Internal Auditor to the Company Under Study

In the following, the researcher explains how to apply the steps of the proposed model for the selection of the internal auditor on the company under study:

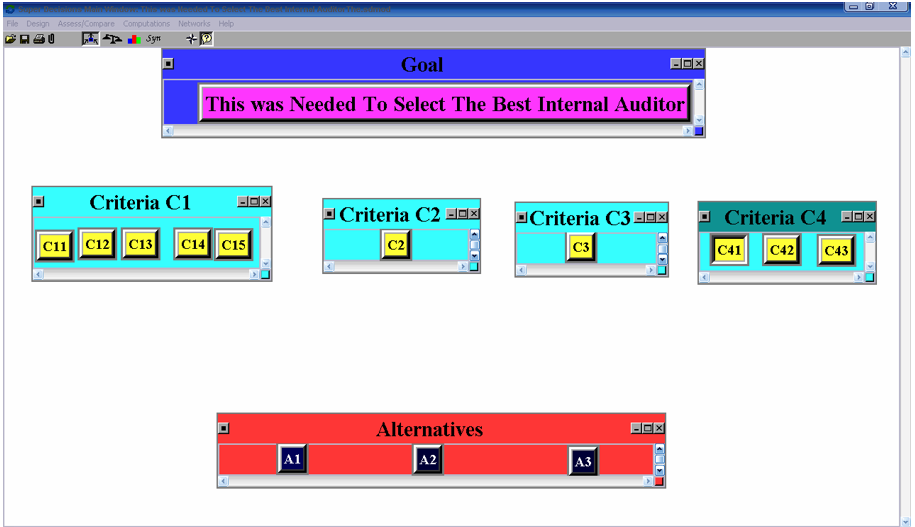

Hierarchical and Network Structure

The Figure 1 shows a picture of the previous codes that were entered in the Super Decisions program to form a hierarchical structure, which is the goal, the main and sub-factors, and the available alternatives:

|

|

|

Figure 1. The goal, the main and sub-factors, and the available alternatives |

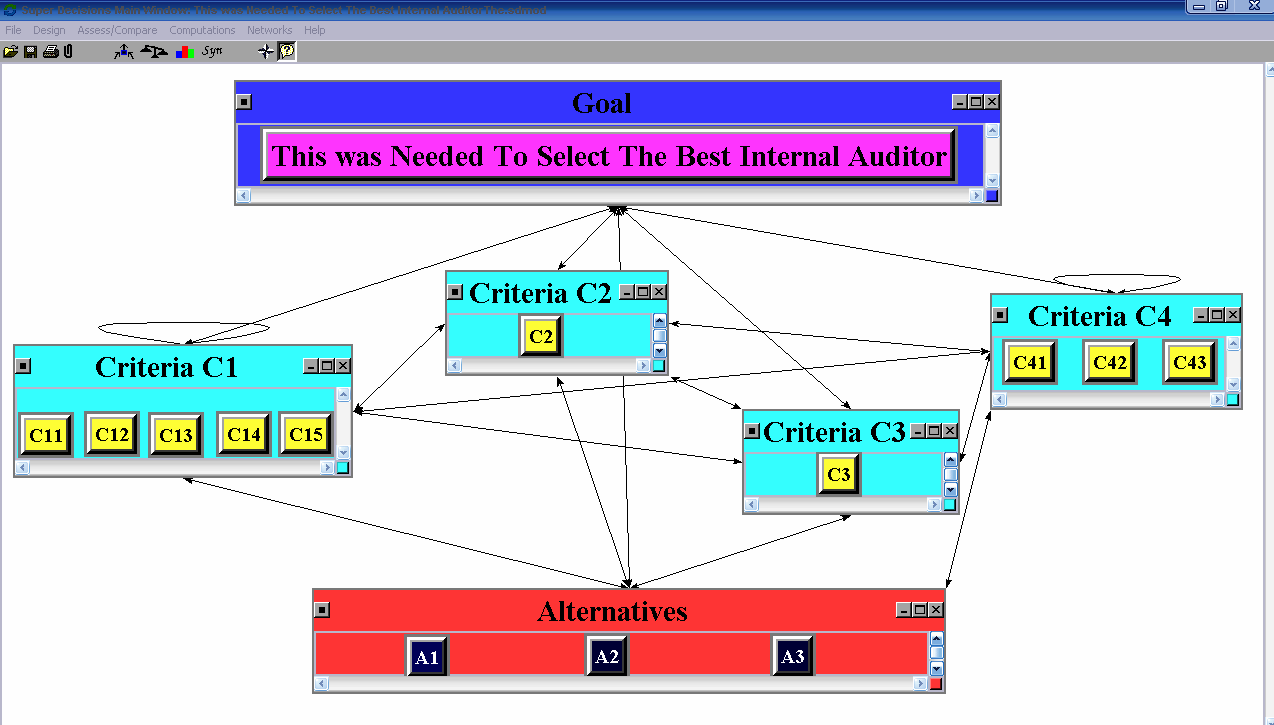

It is clear from the Figure 1 that all the symbols used in the program were presented to express the general goal, the main and subsidiary factors, and the alternatives, but before making the binary comparisons between the factors and each other, and given that the Analytical hierarchy Process suffers from deficiencies represented in that it does not measure the internal relationships between the factors and each other, To avoid this, the integration between the Analytical Network Process and the Analytical hierarchy Process was used to make all the relationships between the factors and each other represented in the main and sub-factors, and by applying this integration in the Super Decisions program, we get the Figure 2:

|

|

|

Figure 2. The integration between the Analytical Network Process and the Analytical hierarchy Process |

Determine the Priority of Each Alternative in Terms of Selection Factors

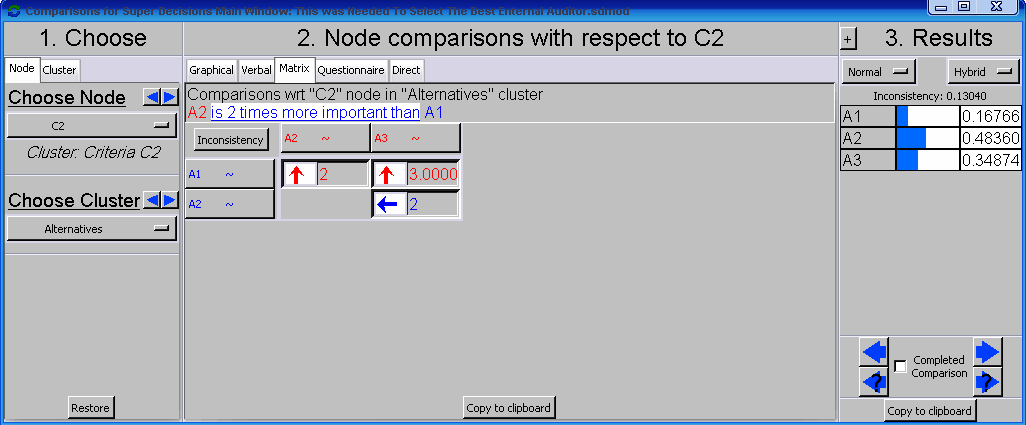

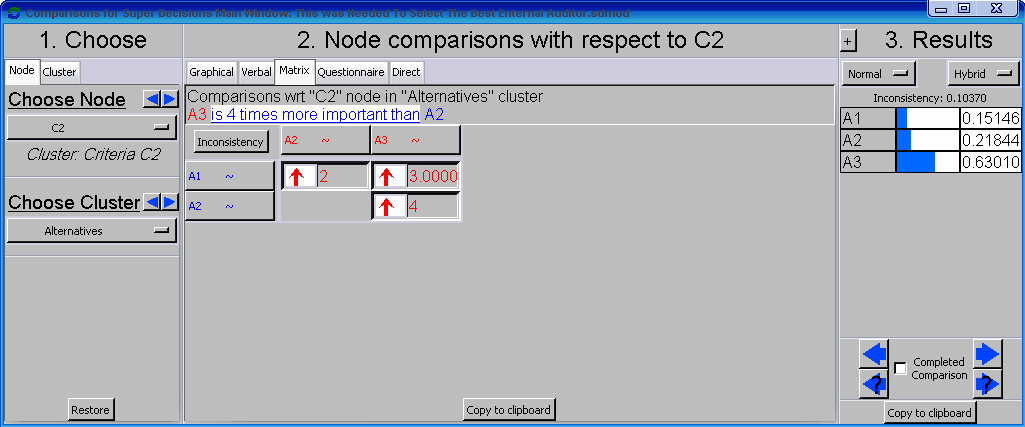

The researcher filled out the matrix of binary comparisons for the alternatives for the selection factors through the data obtained and entered this data into the Super Decisions program, all results of binary comparisons and evaluation of alternatives can be summarized in Table 3:

Table 3. All results of binary comparisons and evaluation of alternatives

|

Alternatives |

Sub-factors |

Main factors |

||

|

A3 |

A2 |

A1 |

||

|

0,29696 |

0,16342 |

0,53961 |

C11 = 0,38771 |

C1 = 0,35365 |

|

0,34874 |

0,16766 |

0,48360 |

C12 = 0,11347 |

|

|

0,44343 |

0,16920 |

0,38737 |

C13 = 0,30014 |

|

|

0,24021 |

0,20984 |

0,54995 |

C14 = 0,12659 |

|

|

0,24931 |

0,15706 |

0,59363 |

C15 = 0,07209 |

|

|

0,34874 |

0,48360 |

0,16766 |

C2 = 0,44375 |

|

|

0,08096 |

0,18839 |

0,73064 |

C3 = 0,12484 |

|

|

0,49339 |

0,19580 |

0,31081 |

C41 = 0,62501 |

C4 = 0,07776 |

|

0,53961 |

0,29696 |

0,16342 |

C42 = 0,23849 |

|

|

0,57143 |

0,28571 |

0,14286 |

C43 = 0,13650 |

|

|

0,3736 |

0,2343 |

0,3920 |

Total |

|

|

the collected values and the order of the alternatives after conducting a sensitivity analysis |

||||

|

0.3955 |

0.2137 |

0.3908 |

Total |

|

From Table 3 it is Clear that

It is clear from the Table 3 that the first factor, which is the qualities and characteristics of the internal auditors, ranked second with a rate of 365,35%, and the second factor, which is impartiality, independence, and objectivity, received the highest importance among the other main selection criteria, with a score of 375,44%, as happened The third factor, which is fees, ranked third with a rate of 484.12%, and the fourth factor, which is the provision of new services according to the contemporary concept of internal audit, ranked fourth, with a rate of 776.7%.

It is clear from the Table 3 that the first sub-factor, which is technical skills, got the first rank with a rate of 771,38%, and the second sub-factor, which is analytical skills, got the fourth rank with a rate of 347.11%, and the third sub-factor, which is personal skills, got the second rank with a rate of 014. 30%, and the fourth sub-factor, which is the skills of dealing with others, ranked third with a rate of 659.12%, and finally, the fifth sub-factor, which is organizational skills, ranked fifth with a rate of 209.7%.

From Table 3 it is clear that The first alternative, Insourcing, ranked first with a rate of 961,53%, The second alternative Outsourcing ranked third with a rate of 342.16% and The third alternative, Co-Sourcing, ranked second with a rate of 696,29%.

From Table 3 it is clear that The first alternative, Insourcing, ranked first with a rate of 360,48%, The second alternative Outsourcing ranked third with a rate of 766,16% and The third alternative, Co-Sourcing, ranked second, with a rate of 874,34%.

From Table 3 it is clear that The first alternative, Insourcing, ranked second, with a rate of 737,38%, The second alternative, Outsourcing, ranked third, with a rate of 920,16% and The third alternative, Co-Sourcing, ranked first with a rate of 343,44%.

From Table 3 it is clear that The first alternative, Insourcing, ranked first with a rate of 995,54%, The second alternative Outsourcing ranked third with a rate of 984.20% and The third alternative, Co-Sourcing, ranked second, with a rate of 021.24%.

From Table 3 it is clear that The first alternative, Insourcing, ranked first with a rate of 363.59%, The second alternative Outsourcing ranked third with a rate of 706,15% and The third alternative, Co-Sourcing, ranked second with a rate of 931,24%.

From Table 3 it is clear that The first alternative Insourcing ranked third with a rate of 766,16%, The second alternative Outsourcing ranked first with a rate of 360,48% and The third alternative, Co-Sourcing, ranked second, with a rate of 874,34%.

From Table 3 it is clear that The first alternative, Insourcing, ranked first with a rate of 064,73%, The second alternative, Outsourcing, ranked second, with a rate of 839.18% and The third alternative, Co-Sourcing, ranked third with a rate of 096.8%.

It is clear from Table 3 that the first sub-factor, which is evaluate the efficacy and improvement of risk management processes, ranked first with a rate of 501.62%, and the second sub-factor, which is evaluate and improve control and governance processes, ranked second with a rate of 849.23%, and the third sub-factor, which is consulting and assurance services ranked third with a score of 650.13%.

From Table 3 it is clear that The first alternative Insourcing ranked second with a rate of 081.31%, The second alternative, e Outsourcing, ranked third, with a rate of 580,19% and The third alternative, Co-Sourcing, ranked first with a rate of 339.49%.

From Table 3 it is clear that The first alternative, Insourcing, ranked third, with a rate of 342.16%, The second alternative, Outsourcing, ranked second, with a rate of 696,29% and The third alternative, Co-Sourcing, ranked first with a rate of 961,53%.

From Table 3 it is clear that The first alternative, Insourcing, ranked third, with a rate of 286,14%, The second alternative, Outsourcing, ranked second, with a rate of 571,28% and The third alternative, Co-Sourcing, ranked first with a rate of 143,57%.

Evaluate the Three Alternatives and Determine the Best Internal Auditor

In this part, each alternative is evaluated in terms of the general objective of selecting the best internal auditor and through the relative weights of the three alternatives in terms of the main and sub-factors for choosing the internal auditor.

Based on the foregoing, the following it is clear from the Table 3 that The first alternative, related to Insourcing, ranked first with a rate of 20.39%, The second alternative, related to Outsourcing, ranked third with a rate of 43.23%and The third alternative, related to Co-Sourcing, ranked second with a rate of 36.37%.

Sensitivity Analysis of the Results of Applying the Proposed Model

It is usually desirable to examine the sensitivity or reaction to a decision as a result of changes in the priorities of the main factors of the problem, by changing the priority of one factor while keeping the priority of the other factors as it is so that the total - including the factor whose ratio we changed - is equal to one once other. To facilitate this examination, the Super Decisions program was designed to give four different ways to display the results of the change in sensitivity (Plot, Barchart, Reichart, Horz Barchart).

The researcher used the Plot map to apply the sensitivity test by applying the second main factor (neutrality, independence, and objectivity).

Figure 3 shows the data entry for the second main factor (impartiality, independence, and objectivity), and thus the arrangement of the available alternatives according to the general model, before conducting a sensitivity analysis:

|

|

|

Figure 3. The arrangement of the available alternatives according to the general model, before conducting a sensitivity analysis |

It is clear from the previous Figure 3 that according to the proposed model for selection, Insourcing is the first, followed by the Co-Sourcing, and finally Outsourcing.

By applying the sensitivity test using the Super Decisions program on the second main factor (impartiality, independence, and objectivity), the relative importance of the second main factor in the proposed model for the third alternative has been increased compared to the second alternative from 1/2 to 4.

Figure 4 shows the data entry for the second main factor (impartiality, independence, and objectivity), and accordingly the order of the available alternatives according to the general model, after conducting a sensitivity analysis:

|

|

|

Figure 4. The arrangement of the available alternatives according to the general model, after conducting a sensitivity analysis |

It is clear from the previous Figure 4 that the alternatives are sensitive to the change in the relative importance of the second main factor (impartiality, independence, and objectivity), as the increase in the relative importance of the second main factor in the proposed model for the third alternative compared to the second alternative from 1/2 to 4 led to a change in the order of the alternatives from what it was the situation before making the change.

Based on the foregoing, the following it is clear from the Table 3 that The first alternative, related to Insourcing, ranked second with a rate of 39.08%, The second alternative, related to Outsourcing, ranked third with a rate of 21.37% and the third alternative, related to Co-Sourcing, ranked first with a rate of 39.55%.

CONCLUSION

The researcher filled the matrix of binary comparisons of alternatives for the selection factors through the data obtained and entered this data into the Super Decisions program, and the matter was as follows:

It is clear from this that the alternatives are sensitive to the change in the relative importance of the second main factor (impartiality, independence, and objectivity), as the increase in the relative importance of the second main factor in the proposed model for the third alternative compared to the second alternative from 1/2 to 4, which led to a change in the order of the alternatives from what it was the situation before making the change.

Recommendations

Future Research Directions

ACKNOWLEDGMENTS: The author would like to thank the Deanship of Scientific Research at Majmaah University for supporting this work under Project Number No. R-2021-328.

CONFLICT OF INTEREST: None

FINANCIAL SUPPORT: The author would like to thank the Deanship of Scientific Research, Majmaah University, Saudi Arabia, for funding this work under project No. R-2021-328.

ETHICS STATEMENT: None

Abbott, L. J., Parker, S., Peters, G. F., & Rama, D. V. (2007). Corporate governance, audit quality, and the Sarbanes‐Oxley Act: Evidence from internal audit outsourcing. The Accounting Review, 82(4), 803-835.

Abdel-Fattah, M. (2001). Outsourcing for the performance of internal audit functions and its impact on the independence of the external auditor and the quality of the audit: a field study. Journal of Accounting Thought, Faculty of Commerce, Ain Shams University, 1, 155-226.

Ahlawat, S. S., & Lowe, D. J. (2004). An examination of internal auditor objectivity: In‐house versus outsourcing. Auditing: A Journal of Practice & Theory, 23(2), 147-158.

Akl, Y. H. (2010). Using the Analytical Hierarchy Process in building a proposed model for selecting the external auditor: An applied study. Journal of Accounting, Management, and Insurance, Faculty of Commerce, Cairo University, 49(77), 827-887.

Al-Adwani, A. M. (2001). Decision support model for choosing a system for Internet services using the Analytical Hierarchy Process. The Arab Journal of Administrative Sciences, Scientific Publication Council - Kuwait University, 8(1), 85-99.

Aldhizer G., Cashell J. D., & Martin D. R. (2003). Internal Audit Outsourcing. The CPA Journal, 73(8), 38-42.

Alghamdi, A., Ibrahim, A., Alraey, M., Alkazemi, A., Alghamdi, I., & Alwarafi, G. (2021). Side effects following COVID-19 vaccination: a cross-sectional survey with age-related outcomes in Saudi Arabia. Journal of Advanced Pharmacy Education and Research, 11(3), 119-125. doi:10.51847/1UfXSzTR6M

Al-Rashed, A. A. A. (2011). Assessment of the opportunities for private sector participation in the completion and development of Iraq’s ports business operations using the Analytical Hierarchy Process (AHP) a field study in the General Company for Iraqi Ports. Journal of Economic Sciences, Iraq, 7(28), 112-158.

Al-Rifai, I. M., (2012). The impact of the source of internal audit activities on the extent to which the external auditor depends on the work of the internal audit - an empirical study. Journal of Commerce and Finance, Faculty of Commerce, Tanta University, 1, 1-43.

Al-Shobaki, I. Y. (2008). Selecting consulting offices using the Analytical Hierarchy Process from the point of view of decision-makers in the Gaza Strip [Unpublished master's thesis]. Islamic University - Gaza.

Bagla, V., Gupta, A., & Mehra, A. (2013). Improving consistency of Comparison matrices in analytical hierarchy process. International Journal of Current Engineering and Technology, 3(2), 316-321.

Bahramuz, A. B. M. A. (2005). Application of the method of Analytical Hierarchy Process of the collective decision to determine the best site for establishing community colleges in the Kingdom of Saudi Arabia. The Saudi Journal of Higher Education, 2, 11-36.

Brandon, D. M. (2010). External auditor evaluations of outsourced internal auditors. Auditing: A Journal of Practice & Theory, 29(2), 159-173.

Brunelli, M. (2015). Introduction to the Analytic Hierarchy Process. Springer Briefs in Operations Research, Cham Heidelberg Dordrecht London New York.

Cheng, E. W., & Li, H. (2004). Contractor selection using the analytic network process. Construction Management and Economics, 22(10), 1021-1032.

Dağdeviren, M., & Yüksel, İ. (2007). Personnel selection using analytic network process. İstanbul Ticaret Üniversitesi Fen Bilimleri Dergisi, 6(11), 99-118.

Daim, T. U., Udbye, A., & Balasubramanian, A. (2013). Use of analytic hierarchy process (AHP) for selection of 3PL providers. Journal of Manufacturing Technology Management, 24(1), 28-51.

El-Garhy, H. A. Kh. H. (2013). Evaluation of the Effectiveness of the Internal Audit Department’s Performance Using the Analytical Hierarchy Process - with an Applied Study [Unpublished doctoral dissertation]. University of Suez Canal.

Elgendy, T. Y. A. A. A. (2015). A proposed model for using the Analytical Hierarchy Process in the selection of internal auditor an applied study. Journal of Accounting Research, Faculty of Commerce, Tanta University, 2, 256-302.

Emara, M. R. A. Gh. (2012). The impact of Outsourcing for the performance of internal auditing on the quality of external auditing: a field study [Unpublished master’s thesis]. University of Cairo.

Farooq, D., & Moslem, S. (2020). Evaluation and ranking of driver behavior factors related to road safety by applying analytic network process. Periodica Polytechnica Transportation Engineering, 48(2), 189-195.

Hadid, A. I. A. (2012). Determining the criteria for selecting the best supplier in the context of the outsourcing process: A case study in the Asiacell Company for cellular communications. International Scientific Conference: Globalization of Management in the Age of Knowledge from 15-17 December (pp. 1-31). Lebanon: Tripoli, University of Al-Jinan.

Hsu, P. F., & Chen, B. Y. (2008). Integrated analytic hierarchy process and entropy to develop a durable goods chain store franchisee selection model. Asia Pacific Journal of Marketing and Logistics, 20(1), 44-54.

Inua, O. I, & Abianga, E. U. (2015). The Effect of the Internal Audit Outsourcing on Auditor Independence: The Nigerian Experience. Research Journal of Finance and Accounting, 6(10), 36-44.

Jeon, J., Kim, J., Park, Y., & Lee, H. (2017). An analytic network process approach to partner selection for acquisition and development. Technology Analysis & Strategic Management, 29(7), 790-803.

Jeong, H. Y. (2020). ANP-based quantification method for the smart manufacturing system design decomposition. The Journal of Supercomputing, 76(8), 6141-6157.

Katarne, R., & Negi, J. (2014). Consistency in the Analytic Hierarchy Process: A Framework for Automobile Steering Technology. International Journal of Engineering Research & Technology (IJERT), 3(5), 559-564.

Kheybari, S., Rezaie, F. M., & Farazmand, H. (2020). Analytic network process: An overview of applications. Applied mathematics and Computation, 367, 124780.

Kyavars, V. (2021). Application of Analytic Network Process: Weighting of Selection Criteria to Select the Suitable Method for the Preparation of Nancrystals. International Journal of Pharmaceutical Sciences and Research (IJPSR), 12(7), 3925-3932.

Lin, H. Y., & Hsu, P. Y. (2007). Application of the analytic hierarchy process on data warehouse system selection decisions for small and large enterprises in Taiwan. International Journal of the Computer, the Internet and Management, 15(3), 73-93.

Mansour, A. M. I. (2007). A critical analytical view of the external performance of internal auditing as one of the sources of business establishments obtaining internal audit services. Journal of Financial and Commercial Studies, Faculty of Commerce, Beni Suef University, (3), 347-397.

MirarabRazi, J., Hassanzad Navrodi, I., Ghajar, I., & Salahi, M. (2020). Identifying optimal location of ecotourism sites by analytic network process and genetic algorithm (GA):(Kheyroud Forest). International Journal of Environmental Science and Technology, 17(5), 2583-2592.

Mohamed, A. Y. Abdel-Fattah. (2004). The impact of the use of Outsourcing in carrying out the tasks of internal auditing: an analytical field study [Unpublished master’s thesis]. University of Suez Canal.

Mujahid, M. A. (2006). Obtaining internal audit activities from an Outsourcing and its impact on the objectivity of internal auditors in light of the environment of variables in professional practice: an empirical study. Journal of Financial and Commercial Studies, College of Commerce, University of Beni Suef, (1), 9-66.

Özdemir, A., Özkan, A., Günkaya, Z., & Banar, M. (2020). Decision-making for the selection of different leachate treatment/management methods: the ANP and PROMETHEE approaches. Environmental Science and Pollution Research, 27(16), 19798-19809.

Percin, S. (2006). An application of the integrated AHP‐PGP model in supplier selection. Measuring Business Excellence, 4(10), 34-49.

Punniyamoorty, M., Mathiyalagan, P., & Lakshmi, G. (2012). A combined application of structural equation modeling (SEM) and analytic hierarchy process (AHP) in supplier selection. Benchmarking: An International Journal, 19(1), 70-92.

Saaty, T. L. (1994). How to make a decision: the analytic hierarchy process. Interfaces, 24(6), 19-43.

Saaty, T. L. (2000). Leaders' Decision Making: The Hierarchical Process of Decisions in a Complex World, translated by Bahramuz, Asmaa bint Muhammad Ahmad and Hamshary, Siham Bint Ali Mohamed, see translation Al-Shawaf, Saeed bin Ali. Kingdom of Saudi Arabia, Riyadh: General Administration of Printing and Publishing, Institute of Public Administration.

Saaty, T. L. (2008). Decision making with the analytic hierarchy process. International Journal of Services Sciences, 1(1), 83-98.

Saaty, T. L., & Vargas, L. G. (2001). How to make a decision. In Models, methods, concepts & applications of the analytic hierarchy process (pp. 1-25). Springer, Boston, MA.

Salem, A. M. K. (2012). The effect of each of the alternatives to Outsourcing for the internal audit function, the assigned party, the type of opinion in the audit reports associated with Outsourcing to the degree of third party reliance on the content of financial reports: an empirical study. The Scientific Journal of Economics and Commerce, Faculty of Commerce, Ain Shams University, 3(2), 719-790.

Sarkis, J., & Seol, I. (2006). An Analytic Network Process Model for Internal Auditor Selection. Applications of Management Science, 12, 215-234.

Seol, I., & Sarkis, J. (2005). A multi‐attribute model for internal auditor selection. Managerial Auditing Journal, 20(8), 876-892.

Shaverdi, M., & Barzin, P. (2012). Applying fuzzy AHP to determination of optimum selection method for economic cocoon traits improvement in silkworm breeding. Business Systems Review, 1(1), 64-84.

Sobeihi, M. H. A. J. (2000). Outsourcing for internal auditing is one of the modern trends in auditing: an analytical study. Journal of Business Research, Faculty of Commerce, Zagazig University, 1, 213-250.

The Institute of Internal Auditor. (2009). Definition of Internal Auditing. Available from: https://na.theiia.org/standards-guidance/Public Documents/IPPF_Definition.doc

Triantaphyllou, E., & Mann, S. H. (1995). Using the analytic hierarchy process for decision making in engineering applications: some challenges. International Journal of Industrial Engineering: Applications and Practice, 2(1), 35-44.

Zandieh, M. (2020). GMP risk assessment at an organic and natural food production plant with emphasis on infrastructure by PHA and FMEA methods. World Journal of Environmental Biosciences, 9(1-2020), 11-15.

Zarei, L., Moradi, N., Peiravian, F., & Mehralian, G. (2020). An application of analytic network process model in supporting decision making to address pharmaceutical shortage. BMC Health Services Research, 20(626). doi:10.1186/s12913-020-05477-y