Accessing credit always appears to be crucial for firms’ development. However, some businesses self-excluded them in the credit markets because of the fear of rejection. The problem is believed to be more severe in underdeveloped countries. With the aim of having a better understanding of the issue, the authors focus on learning potential determinants from firms’ sides in various transition economies, which are always believed to create more obstacles in accessing credit. Using an initial sample of 9,979 observations at firm-level database across 17 transitional economies, we uncover several influences of different elements from the firm’s side in the case of being “discouraged borrowers.” Through the regression results, interesting findings have emerged. Firms’ financial conditions, perceptions, and social capital play a pivotal role in determining the problem. From that viewpoint, managerial implications are made to better support firms to improve their accessibility and lessen the probability of discouragement in the credit market.

INTRODUCTION

Capital is believed to play one of the most important roles in the development of businesses. In the world, firms, especially small and medium ones, often have to struggle to get resources from formal credit channels. Subsequently, enterprises always have the perception that access to financial services is especially difficult in developing countries. This fact leads to the need to find ways to improve the credit access of firms and lessen the case of being rejected.

However, in the credit market, there is always an unbalanced situation between the demanders and suppliers of funds (Akerlof, 1978). As explained, the theory on asymmetric information and lemon problems by Nobel winner Akerlof (1978) is always used. The imperfection in the market makes lenders reluctant to give funds to borrowers, which creates circumstances called credit constraints. To be more specific, the case of credit constraints can normally be divided into two small subsamples: (1) involuntarily excluded and (2) voluntarily excluded in the credit market. Regarding the first, involuntary exclusion comes from being rejected by lenders or being accepted but with a lesser amount of funds. Meanwhile, the latter scenario comes into effect when borrowers (both good and bad) are disqualified or withdraw themselves due to fear of rejection by lenders. In terms of lenders’ perspective, bad borrowers are apparently rationed as they cannot meet the basic requirements. However, if borrowers are of good quality, rationing them could also make lenders suffer from missed opportunities for profitability. Besides, the existence of transaction costs could also be contemplated. If the cost is from higher interest rates and the troublesome application procedures, good borrowers tend to find sources with fewer regulations and exclude from formal channels (Kon & Storey, 2003). Market dysfunction can lead to several negative outcomes, not only for borrowers but also for lenders in particular and the whole economy in general.

In transitional countries, accessing credit is even more severe for firms with a higher level of asymmetric information between borrowers and lenders, greater application and processing costs, and many obstacles from the legislature system, corruption, and bribery. Aware of the problems, we try to add to the literature regarding the involuntary exclusion of borrowers, which are normally known as discouraged borrowers, with the focus on the transitional economies using BEEPS VI databases of WBG-EIB-ERBD, which covers the initial sample of 9,979 observations at firm-level around 16 countries. Our research is trying to fill in the research gap with a synthesis of the literature on determinants of discouraged borrowers and empirical research on several transitional economies in the world. From this viewpoint, we aim to make conclusions on discouraged borrowers and, therefore, suggest several managerial and governance implications.

The rest of the paper is structured as follows. Section 2 represents related literature on discouraged borrowers; Section 3 displays research designs, data collection, variable descriptions, and econometric models. Section 4 commences with explaining the results, and Section 5 concludes with several recommendations.

Literature Review

Overview of Discouraged Borrowers

Long before the term “discouraged borrowers” emerged, Stiglitz and Weiss (1981) mentioned a framework explaining why banks could deny potential borrowers even when they still have adequate funds to lend (Stiglitz & Weiss, 1981). After that, Diagne (1999) explains the situation when firms do not choose to borrow as follows: (1) they do not need funds or (2) they expect to face several limits or high costs of getting capital (Diagne, 1999).

The phrase “discouraged borrowers” was first developed by Kon and Storey (2003). The authors suggest discouraged borrowers as good borrowers excluded themselves in the credit market as they are afraid of being rejected by lenders. It must be noted that there are differences between being discouraged and being constrained. If the first mentioned self-rationing mechanism is from fund demanders, the latter refers to the situation of credit rationing coming from fund suppliers. Even though both cases lead to the inability to access credit, differentiating them has several implications. First and foremost, as for asymmetric information, borrowers are normally gathered into a pooled source, where exists together credible and unreliable ones. As it is hard for lenders to define who is whom and due to numerous unobservable factors, lenders have the tendency to put limits in lending procedures on both types of borrowers, which creates market imperfection. The exclusion of good borrowers in the credit market will have negative consequences for both fund demanders and lenders, which further improve the informal credit channel. In developing countries, this could cause various concerns. Second, differentiating borrowers could help banks and other lenders better access the good fund demanders and help bad ones improve their situation. Consequently, deeper research on the issue could bring fruitful managerial implications.

Determinants of Discouraged Borrowers

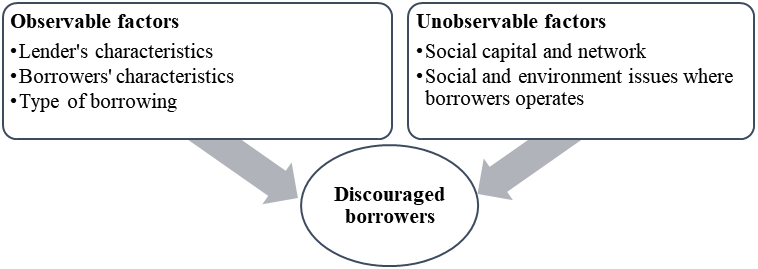

There are a lot of approaches that can be used to evaluate the potential factors affecting discouraged borrowers. Similar to evaluating the accessibility of firms in the credit market, discouraged borrowers are also put into the same context. Empirical studies focus on the characteristics of both lenders and borrowers and the relationships between them, which will be synthesized below. Another way to examine the determinants is that researchers divide them into observable and unobservable ones. Whatever approaches are used, the empirical evidence shows several results in common. After examination, we propose a framework for determinants of discouraged borrowers, as in Figure 1.

|

|

|

Figure 1. Potential factors affecting borrower’s discouragement (Source: Authors’ collection) |

Analyzing from the lender's side, Kon and Storey (2003) propose that banks’ level of screening procedures inadequacy and the spread between banks’ rates and other lenders’ rates are reasons for the level of discouragement. Brown et al. (2011) confirm the results through 8,387 observations at the firm level in 20 different countries across Europe. The type of bank lending could also help explain the case of discouragement for borrowers. Specifically, relationship bank lending is indicated to lessen the problem as it reduces information asymmetry (Berger & Udell, 1998; Berger & Udell, 2006; Chakravarty & Xiang, 2013). Moreover, the foreign ownership structure is also mentioned in literature. The basic notion underlying the results is that foreign banks tend to lend to the bigger firms – the ones with better financial statements, higher levels of transparency, and healthier financial conditions. In addition, countries with lesser development levels with high existence of foreign banks could make the situation of credit discouragement worse (Brown et al., 2022).

Meanwhile, in terms of borrowers’ side, several factors have been put into consideration. As discouraged borrowers could come from the fear of being rejected, borrowers’ perceptions should be paid due attention to. Using a matching database between the SAFE survey and Amadeus, which covers 11,886 firms across European countries, Ferrando and Mulier (2015) point out that the perception of constraints could make the problem severe. Galli et al. (2017) also confirm the existence of the variable and the corruption-fighting policy at the macro level (Galli et al., 2017). Besides, using the 2002/2003 Enterprise Surveys of the World Bank with a focus on 10 developing countries covering 4 continents, Chakravarty and Xiang (2013) show that firms’ characteristics (firm size, firm age), their competition scale and connection between firms and banks and other financial institutions are likely to impact the credit discouragement, which again confirms results presented in various studies such as of Cavaluzzo et al. (2002), Han et al. (2009) (Chakravarty & Xiang, 2013). Elements related to firms’ liquidity, profitability, indebtedness status, ownership structure, and the environment in firms' work can also apparently explain the case as they imply the ability of loan repayment (Cavalluzzo et al., 2002; Han et al., 2009, Mac a Bhaird et al., 2016). The most accepted fact is that, the better firms’ financial conditions, the lesser probability of being discouraged (Ferrando & Mulier, 2015). Innovative activities of a firm are likely to be negatively correlated with credit dissuasion as an adverse perception of rejection and unwillingness to take on added risk. What is more, the negative discernment of economic conditions is in line with positive discouragement (Brown et al., 2022). It must be noted that, when taking all firms’ characteristics into account, mixed findings are shown as some variables can be considered as “stronger” than others in different countries studied.

Last but not least, several impacts from the environment that firms work in are mentioned in several scientific articles. The level of country development, the impact of trust and networks in the regions, corruption, and bribery are elements determining the discouraged borrowers. In less developed countries, problems of being discouraged in credit markets are often witnessed. More specifically, with developing economies, corruption, bribery, and informal gifts still prevail in the market. In this case, informal institutional factors such as social norms, social values, and trust issues play a more important role. McCabe et al. (2003) propose the bank-firm relation is a kind of mutual trust, and SMEs with a higher level of trust from loan managers could enjoy better access to credit, as well as lower probability of being rejected or discouraged (Tang et al., 2017, Tang et al., 2018, Howorth & Moro, 2012, Moro & Fink, 2013, McCabe et al., 2003).

MATERIALS AND METHODS

Study Designs and Data Collection

Using the cross-sectional database, which was retrieved from the BEEPS VI survey, which was taken during 2018-2020 in several countries in the world, we sorted out 16 transitional economies with a total number of 9,979 observations initially. Even though there are several literatures on discouraged borrowers, to our understanding, there are few studies on countries with transitional phases of development. Moreover, with the most recent wave of the BEEPS database by ERBD-WB, the study aims to deliver a more recent view on the issue, especially in the fast-changing globalization and integration with various economic downturns due to external shocks such as COVID-19. The list of countries includes Albania, Bosnia and Hertz, Montenegro, North Macedonia, Serbia, Armenia, Azerbaijan, Belarus, Georgia, Kazakhstan, Kyrgyz Republic, Moldova, Russia, Tajikistan, Uzbekistan and Ukraine. These countries are considered in “transition,” which means that they are changing from post-Soviet Union to more market-oriented countries. As such, the incompletion in infrastructure, regulation, and legislation systems and low level of development are normally witnessed. However, in recent years, transitional countries have experienced various positive changes such as better life satisfaction, positive attitudes of citizens, and more fairness level between males and females in attaining education services. However, corruption still exists, and the institutional trust level of people tends to decrease.

Considering the case of discouraged borrowers, we utilize the concept mentioned by Kon and Storey (2003). We also based on a literature review to add potential variables related to firms’ characteristics in this paper. The list of variables used is shown in part 3.3.

Econometric Models

As the main objective of this paper is to find factors that could have an impact on credit discouragement from the firms’ side, we add on the econometric models with several groups of factors, such as the firms’ characteristics (firm size, establishment type: owned by foreigners, domestic private individuals or State ones, innovation level, the verification of auditors); firms’ financial conditions (the sales and growth of firms); managerial characteristics (gender and experience of managers); firms’ indebtedness status (having informal or informal loans) and social connection (firm-government bonds). The fixed effect on country, sector, and years is also put in the model to make sure that our results are not determined by misplaced variants from specific nations or segments. The main equation is as follows:

|

|

(1) |

As discouraged take binary values, we perform probit regression in most models. Furthermore, we also detangle the case between big and small firms, as well as the ones that have current formal loans or not, to better evaluate the differences between firms. The reason underlying that comes from our understanding that discouraged borrowers often aim at the good ones who are excluded themselves. Big firms are normally considered better borrowers because of their scale while having loans in formal channels means that businesses are successfully going through the screening and monitoring of formal institutions. Both cases can also refer to the “good” companies.

Variables Description

Table 1 illustrates the variables used in the model. According to that, we group them into different categories to better understand the situation of discouraged borrowers. Notably, we only aim at the firms’ perspective in this study.

Table 1. Variable description

|

Variables |

Description and measurement |

|

discouraged |

=1 when facing discouragement; =0 otherwise |

|

Social connection |

|

|

govern-connect |

=1 if having a connection with government; =0 otherwise |

|

Firms’ characteristics |

|

|

perception |

=1 if having a perception of being rejected; =0 otherwise |

|

size |

=1 if firms are big; =0 if firms are SME |

|

foreign_estab |

=1 if being owned mostly by foreigners; =0 otherwise |

|

private_estab |

=1 if being owned mostly by private individuals; =0 otherwise |

|

state_estab |

=1 if being owned mostly by the state or government; =0 otherwise |

|

innovative |

=1 if firms have innovative activities; =0 otherwise |

|

verify |

=1 if being audited by external auditors; =0 otherwise |

|

Managers’ characteristics |

|

|

female |

=1 if the manager is female; =0 otherwise |

|

experience |

Experiences of manager (in years) |

|

Firms’ financial conditions |

|

|

ln-sales |

Natural logarithm of firms’ last sales |

|

sales_growth |

=1 if firms experience increases in sales; =0 otherwise |

|

Firms’ indebtedness situation |

|

|

informal |

=1 if having informal loans; =0 otherwise |

|

formal |

=1 if having formal loans; =0 otherwise |

(Source: Authors’ collection)

With the explanation of variables, we also perform the summary descriptive, which is illustrated in Table 2. It is notable that firms who are discouraged have a higher perception of difficulty in accessing credit through comparing means of non-discouragement and discouragement cases. Furthermore, dejected borrowers tend to have lower financial conditions compared to others.

Table 2. Descriptive summary

|

Variable |

All |

Non-discouraged |

Discouraged |

||||||

|

Obs |

Mean |

STD |

Min |

Max |

Mean |

STD |

Mean |

STD |

|

|

govern-connect |

9,869 |

.205 |

.403 |

0 |

1 |

.279 |

.448 |

.187 |

.392 |

|

perception |

9,705 |

1.208 |

1.312 |

0 |

4 |

1.430 |

1.401 |

2.166 |

1.377 |

|

foreign_estab |

9,897 |

.065 |

.247 |

0 |

1 |

.065 |

.245 |

.045 |

.208 |

|

private_estab |

9,899 |

.906 |

.291 |

0 |

1 |

.896 |

.305 |

.909 |

.287 |

|

state_estab |

9,900 |

.019 |

.137 |

0 |

1 |

.030 |

.171 |

.045 |

.208 |

|

female |

9,896 |

.314 |

.464 |

0 |

1 |

.309 |

.462 |

.308 |

.463 |

|

experience |

9,708 |

16.717 |

22.613 |

1 |

70 |

18.325 |

44.227 |

14.573 |

9.114 |

|

lnsales |

8,679 |

17.359 |

2.980 |

7.6 |

30.7 |

17.992 |

3.040 |

16.583 |

2.469 |

|

sales_growth |

9,453 |

.616 |

.486 |

0 |

1 |

.664 |

.473 |

.581 |

.495 |

|

innovative |

9,899 |

.328 |

.469 |

0 |

1 |

.449 |

.498 |

.195 |

.398 |

|

verify |

9,802 |

.278 |

.448 |

0 |

1 |

.3797 |

.485 |

.240 |

.429 |

|

informal |

9,297 |

21.878 |

30.175 |

0 |

100 |

31.376 |

33.376 |

19.828 |

29.069 |

|

formal |

9,832 |

.339 |

.473 |

0 |

1 |

.791 |

.407 |

.331 |

.472 |

|

size |

9,906 |

.211 |

.408 |

0 |

1 |

.292 |

.456 |

.165 |

.373 |

RESULTS AND DISCUSSION

We run both OLS and Probit at firms on the whole data to have an overall look at the determinants of borrowers’ discouragement. Notably, in both OLS and Probit regression results, similar results emerged (Table 3). As our expectation, the connection between firms and the government shows a negative relation with discouraged. The simple explanation for the case comes from the fact that connection with the State authorities and officials can reduce the problem, as these firms are believed to have a better understanding of how procedures could run, what actions to take, and which hindrances could appear. Firms’ sales, innovation level, and indebtedness status also experience a significant negative coefficient in the regression, which implies that they could reduce the difficulties for borrowers. On the contrary, firms’ perception of the difficulty accessing credit could obstruct them from attracting more capital from the bank and other formal credit sources. The results are consistent with the research of Ferrando and Mulier (2015) and Brown et al. (2022).

Table 3. Multivariate regression on the whole data

|

OLS |

Probit |

|||

|

Robust |

Robust |

|||

|

discouraged |

Coeff. |

SE |

Coeff. |

SE |

|

govern-connect |

-.0225** |

.0105 |

-.286* |

.156 |

|

perception |

.009** |

.0042 |

.121*** |

.042 |

|

foreign_estab |

.008 |

.023 |

-.004 |

.314 |

|

private_estab |

.003 |

.019 |

-.071 |

.258 |

|

state_estab |

.092 |

.039 |

1.210 |

.387 |

|

female |

-.003 |

.011 |

.0249 |

.131 |

|

experience |

-.0001** |

.00004 |

-.0179** |

.007 |

|

lnsales |

-.0106*** |

.004 |

-.111*** |

.036 |

|

sales_growth |

.0081 |

.012 |

.066 |

.127 |

|

innovative |

-.044*** |

.010 |

-.534*** |

.132 |

|

verify |

-.010 |

.010 |

-.081 |

.134 |

|

informal |

-.0002* |

.0001 |

-.004* |

.002 |

|

formal |

-.147*** |

.0197 |

-1.177*** |

.143 |

|

size |

.020 |

.0130 |

.156 |

.192 |

|

Observations |

1,832 |

|

1,611 |

|

|

R-squared |

0.1520 |

|

|

|

|

Pseudo_R2 |

|

|

0.3184 |

|

|

Country FE |

YES |

|

YES |

|

|

Year FE |

YES |

|

YES |

|

|

Industry FE |

YES |

|

YES |

|

*: Significant at 10% level.

**: Significant at 5% level.

***: Significant at 1% level.

(Source: Authors’ collection)

We also perform the regression on firms with different sizes, with results shown in Table 4. Notably, even though the signs of the coefficient from such variables as perception, experience, ln-sales, innovation, informal, and formal appear to be the same across distinctive firm sizes, the level of impact is different. Particularly, the experience of managers, the sales of firms, and having formal loans are more severe for small firms, while innovative activities and perception of difficulty in accessing credit tend to be higher for big firms. This could be explained as follows: bigger firms are likely to undertake more innovations, and the need for credit could be higher. Even bigger ones have more creditworthiness, but they could also fear rejection, as taking more innovations means incremental risk. Markedly, the only negative significant result of informal loans is witnessed in the case of small firms, which confirms the impact of indebtedness status on reducing credit dissuasion but varies across different types of firm size.

Table 4. Regression on discouraged borrowers with several indications

|

Probit |

Big |

Small |

Have formal loan |

No formal loan |

||||

|

Robust |

Robust |

Robust |

Robust |

|||||

|

discouraged |

Coeff. |

SE |

Coeff. |

SE |

Coeff. |

SE |

Coeff. |

SE |

|

govern-connect |

-.360 |

.385 |

-.289 |

.184 |

.107 |

.196 |

-.564** |

.252 |

|

perception |

.171* |

.089 |

.117** |

.048 |

.269*** |

.069 |

.048 |

.064 |

|

foreign_estab |

-1.641 |

.791 |

-.066 |

.393 |

-.469 |

.443 |

-.486 |

.581 |

|

private_estab |

-1.338 |

.772 |

-.082 |

.309 |

-.577 |

.348 |

-.506 |

.524 |

|

state_estab |

.3687 |

.852 |

1.618 |

.627 |

.880 |

.450 |

.632 |

.767 |

|

female |

.3281 |

.313 |

-.077 |

.151 |

.022 |

.190 |

-.019 |

.214 |

|

experience |

-.032** |

.011 |

-.016** |

.008 |

-.013 |

.009 |

-.028** |

.010 |

|

lnsales |

-.147** |

.111 |

-.112** |

.041 |

-.145*** |

.052 |

-.110** |

.055 |

|

sales_growth |

.328 |

.345 |

.029 |

.147 |

.051 |

.173 |

.147 |

.212 |

|

innovative |

-.277** |

.369 |

-.687*** |

.149 |

-.572** |

.208 |

-.742*** |

.221 |

|

verify |

-.012 |

.261 |

-.155 |

.169 |

-.045 |

.160 |

-.186 |

.231 |

|

informal |

-.0004 |

.005 |

-.006** |

.002 |

-.0006 |

.003 |

-.007* |

.004 |

|

formal |

-1.809*** |

.409 |

-1.223*** |

.166 |

|

|

|

|

|

size |

|

|

|

|

.262 |

.253 |

.266 |

.327 |

|

Observations |

316 |

|

1,166 |

|

958 |

|

412 |

|

|

Pseudo R2 |

0.3931 |

|

0.3416 |

|

0.2477 |

|

0.3283 |

|

*: Significant at 10% level.

**: Significant at 5% level.

***: Significant at 1% level.

(Source: Authors’ collection)

Last but not least, for businesses without formal loans, the negative sign of the coefficient is observed, which again confirms that government links could reduce the case of being discouraged. Consequently, Non-formal-loans owners tend to rely on the connections and understanding of the procedures to prevent themselves from discouragement. Lnsales and innovation have a negative significant coefficient with discouraged, confirming our expectations. Experiences of managers and informal loans existence also show a significant negative relation to self-deterrence in credit markets for having having-no-formal-loans businesses, which indicates that in the cases when firms are hard to show they are “good borrowers,” firm-specific characteristics and social capital appear to have more impact.

CONCLUSION

Through the evaluation across 17 transitional economies, the study uncovers several elements that could influence discouraged borrowers. Notably, the perception of being rejected in the credit market has a positive relation with a probability of discouragement. Besides, firms’ financial conditions and innovation level can partially explain the case. Therefore, improving firms’ awareness of credit access should be paid due attention by firms’ managers in particular and policymakers in general. It must be noted that, as different levels of impact could vary between countries and firms, a deeper investigation of factors from the lenders’ side and other unobservable elements should also be put into consideration to gain better insight into the issue.

ACKNOWLEDGMENTS: None

CONFLICT OF INTEREST: None

FINANCIAL SUPPORT: The paper is fully funded by the National Economics University, Hanoi, Vietnam.

ETHICS STATEMENT: None

Akerlof, G. A. (1978). The market for “lemons”: Quality uncertainty and the market mechanism Uncertainty in economics (pp. 235-251): Elsevier.

Berger, A. N., & Udell, G. F. (1998). The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle. Journal of Banking & Finance, 22(6-8), 613-673.

Berger, A. N., & Udell, G. F. (2006). A more complete conceptual framework for SME finance. Journal of Banking & Finance, 30(11), 2945-2966.

Brown, R., Liñares-Zegarra, J. M., & Wilson, J. O. (2022). Innovation and borrower discouragement in SMEs. Small Business Economics, 59(4), 1489-1517.

Cavalluzzo, K. S., Cavalluzzo, L. C., & Wolken, J. D. (2002). Competition, small business financing, and discrimination: Evidence from a new survey. The Journal of Business, 75(4), 641-679.

Chakravarty, S., & Xiang, M. (2013). The international evidence on discouraged small businesses. Journal of Empirical Finance, 20, 63-82.

Diagne, A. (1999). Determinants of household access to and participation in formal and informal credit markets in Malawi.

Ferrando, A., & Mulier, K. (2015). Firms’ financing constraints: Do perceptions match the actual situation? The Economic and Social Review, 46(1, Spring), 87-117.

Galli, E., Mascia, D. V., & Rossi, S. P. S. (2017). Does Corruption Affect the Access to Bank Credit for Micro and Small Businesses? Evidence from European MSMEs ADBI Working Papers (Vol. 756, pp. 1-23): Asian Development Bank Institute (ADBI).

Han, L., Fraser, S., & Storey, D. J. (2009). Are good or bad borrowers discouraged from applying for loans? Evidence from US small business credit markets. Journal of Banking & Finance, 33(2), 415-424.

Howorth, C., & Moro, A. (2012). Trustworthiness and interest rates: an empirical study of Italian SMEs. Small Business Economics, 39, 161-177.

Kon, Y., & Storey, D. J. (2003). A theory of discouraged borrowers. Small Business Economics, 21, 37-49.

Mac an Bhaird, C., Vidal, J. S., & Lucey, B. (2016). Discouraged borrowers: evidence for Eurozone SMEs. Journal of International Financial Markets, Institutions and Money, 44, 46-55.

McCabe, K. A., Rigdon, M. L., & Smith, V. L. (2003). Positive reciprocity and intentions in trust games. Journal of Economic Behavior & Organization, 52(2), 267-275.

Moro, A., & Fink, M. (2013). Loan managers’ trust and credit access for SMEs. Journal of Banking & Finance, 37(3), 927-936.

Stiglitz, J. E., & Weiss, A. J. T. A. e. r. (1981). Credit rationing in markets with imperfect information. 71(3), 393-410.

Tang, Y., Deng, C., & Moro, A. (2017). Firm-bank trusting relationship and discouraged borrowers. Review of Managerial Science, 11, 519-541.

Tang, Y., Moro, A., Sozzo, S., & Li, Z. (2018). Modeling trust evolution within small business lending relationships. Financial Innovation, 4, 1-18.