The article examines the impact of cash flow on the need to increase funding in the Covid pandemic context and the financial constraints of listed companies in Vietnam. We build hypotheses based on the self-ranking match theory framework and research overview. We use data from 5894 observations for 2010-2020 and the general regression model - GLS to test the expected hypotheses. The research results show that cash flow significantly influences the external financing needs of the business. In particular, the cash flow impact and increased need for external financing are more evident in financial constraints and the context of the covid pandemic. The study also shows that the group of companies with financial constraints moved to increase funding when cash flow was in short supply during the Covid pandemic. Besides, the high financial leverage ratio in the previous year can be one of the barriers for businesses that want to access a variety of external financing. The study contributes to the analysis and assessment of the problematic situation of listed companies. In the future, this study can be extended when approaching businesses in the financial sector and evaluating other macro factors that can affect the capital sources of enterprises.

INTRODUCTION

Raising outside capital to increase business operations finance plays an important role. (Modigliani & Miller, 1958) assumed that in a perfect capital market with no costs, a firm's investment decisions are independent of its financial condition because external financing is a perfect substitute for the internal capital of the business, and the cost of using these funding sources is the same. However, businesses often face many limitations when exposed to external funding. Therefore, raising capital from these sources will be heavily influenced by other factors, including cash flow and financial constraints (Faulkender & Petersen, 2006).

Meanwhile, under the covid 19 pandemic influence, the difficulties in accessing external financing for enterprises are increasing (Baker et al., 2020). The number of bankrupt enterprises increased along with the decrease in business results. Internal capital is insufficient to maintain enterprises' production and business activities, and there is a need to consider new funding sources.

The article studies the impact of cash flow on businesses' increased need for external funding, specifically when the covid pandemic and financial barriers impact businesses. All models in this study are estimated on disaggregated samples of financial constraints by firm size. We use 5894 observations of companies listed on the Vietnamese stock market from 2010 to 2020.

Research results show that the impact of the covid pandemic has a considerable impact on corporate funding. When retained earnings extracted from cash flows from production and business activities are not enough to finance investment decisions, Vietnamese companies often tend to increase external financing. The substitution effect of cash flow with an increased need for external financing will be more evident in financially constrained firms. At the same time, when considering the variable that represents the interacting factors between cash flow and COVID factors, companies with financial constraints tend to increase the use of funding during the pandemic-affected period. COVID.

Our research contributes to the external financing theory based on two aspects. Firstly, this is the first study to examine the impact of covid on listed companies in Vietnam in the context of seeking external funding. The built models are meant for businesses to assess the situation and find better recommendations in the epidemic context. Second, financial constraints are assessed and reviewed simultaneously under the impact of the covid pandemic. These assessments will be essential for businesses when controlling cash flow and limiting financial risks to attract capital for better production and business activities.

Literature Reviews and Hypotheses

Modern corporate finance theory acknowledges the influence of internal funding on a firm's access to and propensity to use external financing (López-Gracia & Sogorb-Mira, 2014; Damanhouri et al., 2021). According to the tradeoff capital structure theory, firms with abundant cash flows will pursue a highly leveraged policy to obtain a return on the interest tax shield.

Using the perspective of pecking order theory, (Almeida & Campello, 2010; Kanathila et al., 2021) hypothesized the negative correlation between internal funding and external funding under the influence of defects of markets, such as information asymmetry or moral hazard. Specifically, information asymmetry is one of the causes of financial constraints. At the same time, information asymmetry can also explain the difference between internal and external financing costs. This interpretation is based on the views of many earlier scholars. They argue that managers know more inside information about the company's performance and potential investment opportunities than outside shareholders and creditors (Myers, 1984). Meanwhile, by emphasizing the effects of information asymmetry, pecking order theory predicts a negative correlation between cash flow and external financing; In other words, companies will tend to choose funding sources in descending order of priority, starting from internal funding, then financing by debt, and finally issuing shares (Shyam-Sunder & Myers, 1999).

In addition, many previous studies have emphasized the role of financial barriers in a firm's ability to seek and choose to use external financing (Faulkender & Petersen, 2006). Specifically, most scholars support the view that financial constraints are one of the reasons for the difference between the cost of using internal funding and the cost of using external funding, thereby affecting the company's funding decisions (Almeida & Campello, 2010; Chen & Hsiao, 2014; López-Gracia & Sogorb-Mira, 2014; Park, 2019). As a result, financially constrained firms have fewer funding options and higher external financing costs than unconstrained firms (Carpenter & Petersen, 2002; Almeida & Campello, 2010).

Based on the self-ranking match theory framework and research overview, we build two hypotheses as follows:

Hypothesis 1: Cash flow significantly affects a firm's need for external financing.

Hypothesis 2: Cash flow effects and increased need for external financing will be more pronounced in constrained financial conditions.

The COVID pandemic is one of the reasons why profits from production and business activities become unstable. Financially constrained companies are more likely to face shocks in cash flow, forcing this group of companies to access other funding sources to make up for this shortfall and finance support investment decisions. The companies have been heavily affected by the COVID-19 pandemic in Vietnam and the world since 2020. During this period, many companies faced difficulties in production and business activities; therefore, retained earnings from operating cash flows may not be enough to finance investment decisions and force the company to raise additional external funding. This impact is expected to be more pronounced for financially constrained companies – the group that has to face shocks due to the impact of the pandemic. At the same time, the COVID-19 pandemic is assessed as a risk-triggering event. (Baker et al., 2020) states that no previous infectious disease, including the Spanish flu, has impacted the stock market as strongly as the COVID-19 pandemic. (Yan et al., 2020), analyze the potential effects of the coronavirus, COVID-19, on the stock market, and suggest possible ways an individual can profit from the market affected by the global virus outbreak. In addition, the impact of the covid pandemic on business performance (Dang Ngoc et al., 2021). The business's cash flow will be affected, which will lead to a significant decrease in capital funding for businesses, so we develop the following two hypotheses:

Hypothesis 3: In the context of the covid pandemic, cash flow affects the need for more considerable external funding.

Hypothesis 4: In the context of the covid pandemic and financial constraints, the impact of cash flows on external financing is more significant and pronounced.

MATERIALS AND METHODS

Inheriting the research method of (Almeida & Campello, 2010) and (López-Gracia & Sogorb-Mira, 2014), this study uses two research models to test the hypotheses. Specifically, the model establishes additional financing needs as a function of cash flow, cash holdings, company size, and convertible assets.

Model 1: Consider the effect of cash flow on external financing of the companies described as follows:

|

EXTFINit = b0+ b1CFit + λ1CASH i(t-1) + λ2LEVi(t-1) + λ3SIZE it + λ4COLLAT i(t-1) + eit |

(1) |

EXTFINit is the dependent variable representing the additional external financing needs of a company i at year t, CFit is the independent variable representing the cash flow of company i at year t. Control variables SIZEit firm size, CASH i(t-1) representing the previous year's cash and cash equivalents, LEVi(t-1) representing the previous year's financial leverage, and assets convertible into cash prior to year COLLAT i(t-1)). The variables in model 1 are presented in Table 1.

Model 2: Consider the impact of COVID and the effect of cash flow on the external financing of the companies described as follows:

|

EXTFINit = b0 + b1CFit + b2COVIDit + b3COVID_CFit + λ1CASH i(t-1) + λ2LEVi(t-1) + λ3SIZE it + λ4COLLAT i(t-1) + eit |

(2) |

COVIDit is a dummy variable for data belonging to 2020, which is the year of the impact of the COVID pandemic; The variable COVID_CFit is an interaction variable between the COVID pandemic and cash flow (CF).

In both model 1 and model 2, we will consider enterprises' financial constraints and how cash flow affects external financing. To achieve the research objective of testing the impact of financial constraints on the relationship between cash flow and external financing for listed companies in Vietnam, all models in this study are estimated on disaggregated samples of financial constraints by firm size. Inheriting (Park's, 2019) method, we rank companies by size from small to large into quintiles and, at the same time, identify companies with sizes below the 1st percentile as the group of companies that are the most severe financial constraints. Similarly, firms in the upper 4th percentile in size would be classified as virtually unconstrained firms. The value of firm size is reflected in the book value of total assets – one of the standard measures of identifying financial constraints (Fama & French, 2002).

Table 1. Summary of variables in the research model

|

Variables |

Symbols and Measurements |

Pre-research |

Expectations |

|

Dependent variable |

|||

|

External financing |

EXTFINit = EXTFIN_Dit + EXTFIN_Eit |

(Myers, 1984; Almeida & Campello, 2010; López-Gracia & Sogorb-Mira, 2014; Park, 2019) |

|

|

External financing with debt |

EXTFIN_Dit = (Liabilities – Liabilitiesi(t-1)) /Total assetsit |

||

|

External financing with equity |

EXTFIN_Eit =(Equity – Equityi(t-1)) /Total Assetsit |

||

|

Independent variables |

|||

|

Cash flow |

CFit = (Net Profitit + Depreciationit)/Total Assetsit |

_ |

|

|

Control variables |

|||

|

Cash and cash equivalents |

CASHit = (Cash and cash equivalentsi(t-1))/Total assetsi(t-1) |

(Almeida & Campello, 2010; López-Gracia & Sogorb-Mira, 2014) |

+ |

|

Debt ratio |

LEVit = Total liabilitiest-1/Total assetst-1 |

- |

|

|

Company size |

Ln (Total assetsit) |

+ |

|

|

Assets convertible into money |

COLLATit = (Inventoryt-1+ Accounts Receivablet-1+ Fixed assetsi(t-1))/Total assetsi(t-1) |

(Almeida & Campello, 2010; López-Gracia & Sogorb-Mira, 2014) |

+ |

Previous scholars often used fixed effects regression models (FEM), random effects regression models (REM) (López-Gracia & Sogorb-Mira, 2014) and (Park, 2019), or Generalized Method of Moments (GMM) (Almeida & Campello, 2010) and (Chen & Hsiao, 2014), to test the influence of cash flow on external financing in firms. However, we realized that GLS is suitable for the research data's objectives and characteristics, so we used the general regression model to test the hypotheses. The GLS estimation method limits the problem of autocorrelation and variable variance.

The study uses 5894 observations of companies listed on the Vietnamese stock market from 2010 to 2020. The data is taken from audited financial statements (balance sheet, income statement, and cash flows) and organized as tabular data.

RESULTS AND DISCUSSION

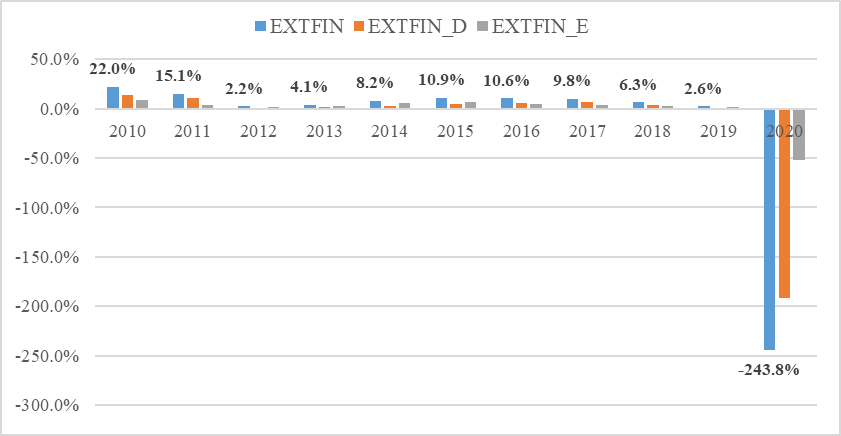

According to Figure 1, the average funding source of enterprises from 2010 to 2019 has grown. In 2010, the growth rate of funding was 22%, of which external financing accounted for 13.6%, from the equity of 8.4%; by 2019, the growth rate of funding was low at only 2.6%. In particular, under the influence of the covid pandemic, funding severely declined by 243.8%, of which funding from external debt decreased by 192% in 2020, and funding from equity sources decreased by 51.8%. Thus, the impact of the covid pandemic significantly impacts the funding of businesses.

|

|

|

Figure 1. External financing variation |

The author performed descriptive statistical analysis to clarify the characteristics of the data. The outliers greatly influence the accuracy of the models, so we clean the data by removing outliers of all variables at the 1% level in both distribution tails. Statistical results describe the independent and dependent variables. The two tables below summarize the control variables, including the number of observations, mean, median, standard deviation, and maximum and minimum values.

Table 2. Descriptive Statistics

|

Variable |

Obs |

Mean |

Std.Dev |

Min |

Max |

|

EXTFIN |

5,984 |

-0.014 |

3.307 |

-198.766 |

1.904 |

|

EXTFIN_D |

5,984 |

-0.033 |

2.555 |

-153.424 |

1.898 |

|

EXTFIN_E |

5,984 |

0.019 |

0.768 |

-45.341 |

0.969 |

|

CF |

5,984 |

0.088 |

0.130 |

-1.748 |

5.085 |

|

CASH |

5,984 |

0.099 |

0.112 |

0.000 |

0.961 |

|

LEV |

5,984 |

0.495 |

0.222 |

0.001 |

0.993 |

|

SIZE |

5,984 |

27.181 |

1.545 |

23.330 |

33.677 |

|

COLLAT |

5,984 |

0.652 |

0.219 |

0.001 |

1.000 |

The descriptive statistical analysis results in Table 2 show that in the 11 years of research from 2010 to 2020, the data sample of businesses without financial constraints includes 5984 observations. The mean column of the research variables shows that the average value of debt is -0.033. Next, the average value of funding from equity issuance in companies is 0.019. In the results of companies that use external financing simultaneously from debt and new equity issues, the mean is -0.014. Thus, the above data shows that, in Vietnam, both businesses use more financing from equity issuance than debt, similar to the descriptive statistics of the Spanish market in the study by (López-Gracia & Sogorb-Mira, 2014). Next, we assume the cash flow variable CF; the average value of CF in the group of unlisted firms is 0.088.

First, the explanatory variable CF, and the dependent variable EXTFIN, are negatively correlated at the significance level. When the cash flow decreases, these companies will mobilize more from outside to make up for the shortfall in cash flow and, vice versa, reduce the use of the above capital sources when the business's cash flow increases. With the previous year's money, cash equivalents (CASH) variable, the author only found a positive correlation with the dependent variable EXTFIN but not significant. Although no correlation was found between CASH and the other dependent variable, EXTFIN, the results also imply that listed companies holding more cash are less likely to increase external financing from debt to finance capital cost savings and vice versa. LEV has a negative relationship with the EXTFIN variable for the financial leverage factor. At the same time, the firm size (SIZE) positively correlates with all three EXTFIN-dependent variables and is statistically significant. Therefore, the larger the listed companies, the more funding they receive from outside than the small ones. Finally, there is no clear correlation between COLLAT and EXTFIN.

Table 3. Correlation Matrix

|

EXTFIN |

CF |

CASH |

LEV |

SIZE |

COLLAT |

|

|

EXTFIN |

1 |

|||||

|

CF |

-0.4137* |

1 |

||||

|

CASH |

0.0154 |

0.1860* |

1 |

|||

|

LEV |

-0.0314* |

-0.1878* |

-0.2566* |

1 |

||

|

SIZE |

0.0630* |

-0.0544* |

-0.1089* |

0.3025* |

1 |

|

|

COLLAT |

-0.0125 |

-0.0299* |

-0.3773* |

0.3794* |

-0.0644* |

1 |

t statistics in brackets * p<0.05

In Table 3, all three columns have a negative sign and have a statistical significance of 1%, which shows that most Vietnamese companies tend to increase external financing. The correlation obtained between the explanatory variable (CF) and the dependent variables (EXTFIN) in this study is similar to the research conclusion of (Almeida & Campello, 2010; Chen & Hsiao, 2014; López-Gracia & Sogorb-Mira, 2014; Park, 2019).

In summary, the regression results obtained from model 1 and model 2 confirm that the results in the baseline models are solid, even when adding control variables to the model. The results in both models show the effect of cash flow on external financing of listed companies in Vietnam.

Table 4. Regression results of model 1 & model 2

|

|

Model 1 |

Model 2 |

||||

|

EXTFIN |

EXTFIN_D |

EXTFIN_E |

EXTFIN |

EXTFIN_D |

EXTFIN_E |

|

|

CF |

-11.49*** |

-9.139*** |

-2.354*** |

|

|

|

|

[-37.83] |

[-39.24] |

[-32.49] |

|

|

|

|

|

COVID |

|

|

|

0.647*** |

0.458*** |

0.189*** |

|

|

|

|

|

[3.54] |

[3.25] |

[4.35] |

|

COVID_CF |

|

|

|

-21.66*** |

-16.41*** |

-5.255*** |

|

|

|

|

|

[-40.05] |

[-39.44] |

[-40.87] |

|

CASH |

2.958*** |

2.324*** |

0.634*** |

0.49 |

0.451* |

0.0391 |

|

[7.81] |

[8.00] |

[7.01] |

[1.45] |

[1.73] |

[0.49] |

|

|

LEV |

-2.224*** |

-1.794*** |

-0.430*** |

-0.746*** |

-0.676*** |

-0.0699 |

|

[-10.94] |

[-11.51] |

[-8.86] |

[-4.07] |

[-4.80] |

[-1.60] |

|

|

SIZE |

0.212*** |

0.170*** |

0.0429*** |

0.125*** |

0.104*** |

0.0213*** |

|

[7.96] |

[8.28] |

[6.73] |

[5.27] |

[5.68] |

[3.77] |

|

|

COLLAT |

1.132*** |

0.915*** |

0.217*** |

0.242 |

0.240* |

0.00212 |

|

[5.51] |

[5.81] |

[4.43] |

[1.33] |

[1.71] |

[0.05] |

|

|

_cons |

-4.704*** |

-3.773*** |

-0.931*** |

-3.144*** |

-2.601*** |

-0.543*** |

|

[-6.34] |

[-6.63] |

[-5.26] |

[-4.78] |

[-5.14] |

[-3.48] |

|

|

N |

5984 |

5984 |

5984 |

5984 |

5984 |

5984 |

t statistics in brackets * p<0.1, ** p<0.05, *** p<0.01

For control variables, the results of Table 4 show that all factors affect funding and have statistical significance at 1%, in which the influence on external financing from debt is more significant for equity financing. Specifically, the factor of cash and cash equivalents (CASH) in the previous year and convertible assets to cash (COLLAT) in the previous year has a positive relationship with the increased demand for financing in general and external financing. This result implies that Vietnamese companies still use external financing when holding a lot of cash and convertible assets. The results observed by CASH the previous year in this study agree with the results of (Chen & Hsiao, 2014) but not with the results of Gracia & Mira (2014). The reason is that the profit from the interest tax shield is enough to offset the loss Vietnamese companies have to incur from the cost of capital of debt financing.

Similarly, the results observed for COLLAT the previous year in all columns agree with the results in the study (Chen & Hsiao, 2014). In contrast with the results of (López-Gracia & Sogorb-Mira, 2014), this difference can be understood that instead of selling convertible assets to get money to finance investment decisions, Vietnamese companies often use those assets as their collateral for their loans. Last year's financial leverage ratio (LEV) negatively correlated with the funding need for companies with high prior-year financial leverage. LEV can be one of the barriers when companies want to access external financing because investors will be anxious about these companies' ability to repay their debts. Research results are similar to those of (Almeida & Campello, 2010; López-Gracia & Sogorb-Mira, 2014).

Focusing on samples classified as financial constraints by size, most of the coefficients before cash flow (CF) are negative and statistically significant from 1%, 5%, and 10%; this reflects the increasing trend of external financing of Vietnamese companies when the available internal sources are not sufficient to finance investment projects. The regression coefficient of CF in the group of financially constrained firms (group 1 - Highest financial constraint group) is much higher than in unconstrained firms, indicating that financially constrained firms are more likely to increase external financing than external financing in unconstrained firms.

Table 4 presents the results of the second model analyzing the impact of cash flows on external financing for listed companies in Vietnam during the COVID pandemic. The correlation coefficient of cash flow (CF) with external and non-debt financing is negative but not statistically significant, while cash flow (CF) has an increasingly positive relationship. External financing of Vietnamese companies when retained earnings from cash flow from production and business activities are not enough to finance investment projects. The COVID pandemic factor has a positive and statistically significant effect at 1% for debt financing and retained earnings financing. The regression coefficient of the interaction variable between COVID_CF has a vast and significant impact on funding. The impact on external financing from liabilities is more significant than financing from retained earnings. Thus, the regression results from the study show that cash flow exhibits a negative correlation with increased demand for both external and internal funding and the substitution effect between cash flow and internal funding. The increased need for external financing will be attributed mainly to the impact of the COVID pandemic, so the third hypothesis is accepted.

Table 5. Regression results of model 1 under financial constraints

|

By scale |

||||||

|

Financial constraints |

No Financial constraints |

|||||

|

Quantile 1 |

Quantile 2 |

Quantile 3 |

Quantile 4 |

Quantile 5 |

||

|

CF |

-19.43*** |

-0.332* |

0.439*** |

0.01 |

-0.271** |

|

|

[-24.28] |

[-1.69] |

[3.00] |

[0.06] |

[-2.11] |

||

|

CASH |

4.872*** |

0.18 |

0.08 |

0.13 |

-0.03 |

|

|

[3.33] |

[0.98] |

[0.45] |

[1.11] |

[-0.30] |

||

|

LEV |

-3.807*** |

-0.678*** |

-0.254*** |

-0.122** |

-0.171*** |

|

|

[-4.07] |

[-6.14] |

[-2.98] |

[-2.41] |

[-3.31] |

||

|

SIZE |

0.808*** |

0.1 |

0.11 |

-0.01 |

0.01 |

|

|

[3.03] |

[1.00] |

[1.60] |

[-0.29] |

[0.71] |

||

|

COLLAT |

2.015** |

0.229** |

0.03 |

-0.07 |

-0.04 |

|

|

[2.20] |

[2.01] |

[0.39] |

[-1.35] |

[-0.94] |

||

|

_cons |

-19.17*** |

-2.44 |

-2.86 |

0.52 |

0.1 |

|

|

[-2.88] |

[-0.94] |

[-1.52] |

[0.51] |

[0.35] |

||

|

N |

1197 |

1197 |

1197 |

1197 |

1196 |

|

The result in Table 5 is similar to the results of Almeida & Campello (2010); Gracia & Mira (2014); JinPark (2019). When the business activities are not enough to finance investment decisions, Vietnamese companies tend to increase external financing. The substitution effect of cash flow with additional external financing will be more evident in financing-constrained firms.

In Table 6, COVID exhibits a negative correlation with the coefficient with the increased funding needs of financially constrained firms and does not show any correlation or positive correlation with the case of unconstrained firms, implying that only financially constrained firms tend to increase the use of financing over time impacted by the COVID pandemic. The performance of small-scale companies has decreased significantly during the time of impact due to the covid pandemic. As a result, these companies were forced to mobilize additional external financing to fill the shortfall in cash flow. The regression coefficient of COVID_CF is significantly negative in the 1st percentile of the 2nd percentile (Financially constrained group) and not statistically significant in the remaining groups, indicating that the group of companies that is financially constrained tend to increase funding when the cash flow is in short supply during the Covid pandemic. The results obtained from model 2 for firms using debt and equity financing were also observed in the case of firms using financing. In summary, the results obtained from model 2 complement the fourth hypothesis in this study, specifically in the period of impact of the covid pandemic, companies tend to increase external financing.

Table 6. Regression results of model 2 covid effects according to financial constraints

|

By scale |

||||||

|

Financial constraints |

No Financial constraints |

|||||

|

Quantile 1 |

Quantile 2 |

Quantile 3 |

Quantile 4 |

Quantile 5 |

||

|

CF |

-0.29 |

0.536*** |

0.434*** |

0.07 |

-0.274** |

|

|

[-0.17] |

[2.61] |

[3.01] |

[0.53] |

[-2.08] |

||

|

COVID |

-10.19*** |

-1.554*** |

-0.511*** |

0.114** |

-0.06 |

|

|

[-7.91] |

[-12.00] |

[-4.35] |

[1.96] |

[-1.08] |

||

|

COVID_CF |

-20.42*** |

-1.939*** |

-0.71 |

-0.846* |

0.15 |

|

|

[-10.59] |

[-4.76] |

[-0.63] |

[-1.78] |

[0.31] |

||

|

CASH |

1.03 |

-0.06 |

0.03 |

0.13 |

-0.04 |

|

|

[0.76] |

[-0.37] |

[0.16] |

[1.09] |

[-0.40] |

||

|

LEV |

-1.18 |

-0.543*** |

-0.306*** |

-0.114** |

-0.176*** |

|

|

[-1.36] |

[-5.40] |

[-3.64] |

[-2.23] |

[-3.40] |

||

|

SIZE |

0.27 |

0.07 |

0.112* |

-0.01 |

0.01 |

|

|

[1.09] |

[0.79] |

[1.65] |

[-0.26] |

[0.87] |

||

|

COLLAT |

0.09 |

0.14 |

0.01 |

-0.08 |

-0.04 |

|

|

[0.11] |

[1.34] |

[0.16] |

[-1.44] |

[-0.92] |

||

|

_cons |

-6.46 |

-1.69 |

-2.81 |

0.48 |

0.06 |

|

|

[-1.04] |

[-0.72] |

[-1.53] |

[0.48] |

[0.21] |

||

|

N |

1197 |

1197 |

1197 |

1197 |

1196 |

|

CONCLUSION

This study evaluates the impact of cash flow on external financing of listed companies in Vietnam for ten years (2010-2020). The research team used the general regression model - GLS to test the expected hypotheses. The results show that external financing from debt is more considerable than financing from equity. The previous year's cash and cash equivalents (CASH) and convertible assets (COLLAT) in the previous year have a positive relationship with the increased demand for public and external financing. This result implies that Vietnamese companies still use external financing when holding a lot of cash and convertible assets. Besides, the previous year's financial leverage ratio (LEV) was negatively correlated with funding demand. A high prior-year financial leverage ratio can be one of the barriers when companies want to access external financing. In addition, the study also shows that the group of companies with financial constraints tend to increase funding when cash flow is in short supply during the Covid pandemic.

In the future, this study can be extended when approaching businesses in the financial sector and evaluating other macro factors that can affect the capital sources of enterprises. In addition, policies to support businesses to restore production and business activities due to Covid-19 are also a matter of concern.

ACKNOWLEDGMENTS: The article came into being within project no. CBQT2.2020.29/QD-DHKTQD, National Economics University, 2020.

CONFLICT OF INTEREST: The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

FINANCIAL SUPPORT: This work was financed by National Economics University, Vietnam.

ETHICS STATEMENT: None

Almeida, H., & Campello, M. (2010). Financing frictions and the substitution between internal and external funds. Journal of Financial and Quantitative Analysis, 45(3), 589-622.

Baker, S. R., Bloom, N., Davis, S. J., Kost, K., Sammon, M., & Viratyosin, T. (2020). The unprecedented stock market reaction to COVID-19. Covid Economics: Vetted and Real-Time Papers, 1(3).

Carpenter, R. E., & Petersen, B. C. (2002). Is the growth of small firms constrained by internal finance? Review of Economics and Statistics, 84(2), 298-309.

Chen, N., & Hsiao, E. (2014). Insider ownership and financial flexibility. Applied Economics, 46(29), 3609-3629.

Damanhouri, Z. A., Alkreathy, H. M., Ali, A. S., & Karim, S. (2021). The potential role of fluoroquinolones in the management of Covid-19 a rapid review. Journal of Advanced Pharmacy Education and Research, 11(1), 128-134. doi:10.51847/FE1iOIPTwD

Dang Ngoc, H., Vu Thi Thuy, V., & Le Van, C. (2021). Covid 19 pandemic and Abnormal Stock Returns of listed companies in Vietnam. Cogent Business & Management, 8(1), 1941587.

Fama, E. F., & French, K. R. (2002). Testing tradeoff and pecking order predictions about dividends and debt. The Review of Financial Studies, 15(1), 1-33.

Faulkender, M., & Petersen, M. A. (2006). Does the source of capital affect capital structure? The Review of Financial Studies, 19(1), 45-79.

Kanathila, H., Peter, M., Bembalagi, M., & Jaiswal, R. S. (2021). Awareness towards personal protective equipment among dental professionals in India during Covid-19 outbreak- a survey. Annals of Dental Specialty, 9(3), 82-88. doi:10.51847/n1FMH7VKZ7

Kaplan, S. N., & Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics, 112(1), 169-215. doi:10.1162/003355397555163

López-Gracia, J., & Sogorb-Mira, F. (2014). Sensitivity of external resources to cash flow under financial constraints. International Business Review, 23(5), 920-930.

Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. The American Economic Review, 48(3), 261-297.

Myers, S. C. (1984). Capital structure puzzle. NBER Working Paper(w1393).

Park, J. (2019). Financial constraints and the cash flow sensitivities of external financing: Evidence from Korea. Research in International Business and Finance, 49, 241-250.

Shyam-Sunder, L., & Myers, S. C. (1999). Testing static tradeoff against pecking order models of capital structure. Journal of Financial Economics, 51(2), 219-244.

Yan, B., Stuart, L., Tu, A., & Zhang, T. (2020). Analysis of the Effect of COVID-19 on the Stock Market and Potential Investing Strategies. Available at SSRN 3563380.